Mordor Intelligence’s new study on the “Leather Chemicals Market Size” presents a thorough evaluation of the market's trajectory, including major trends and future outlook.

Market Overview:

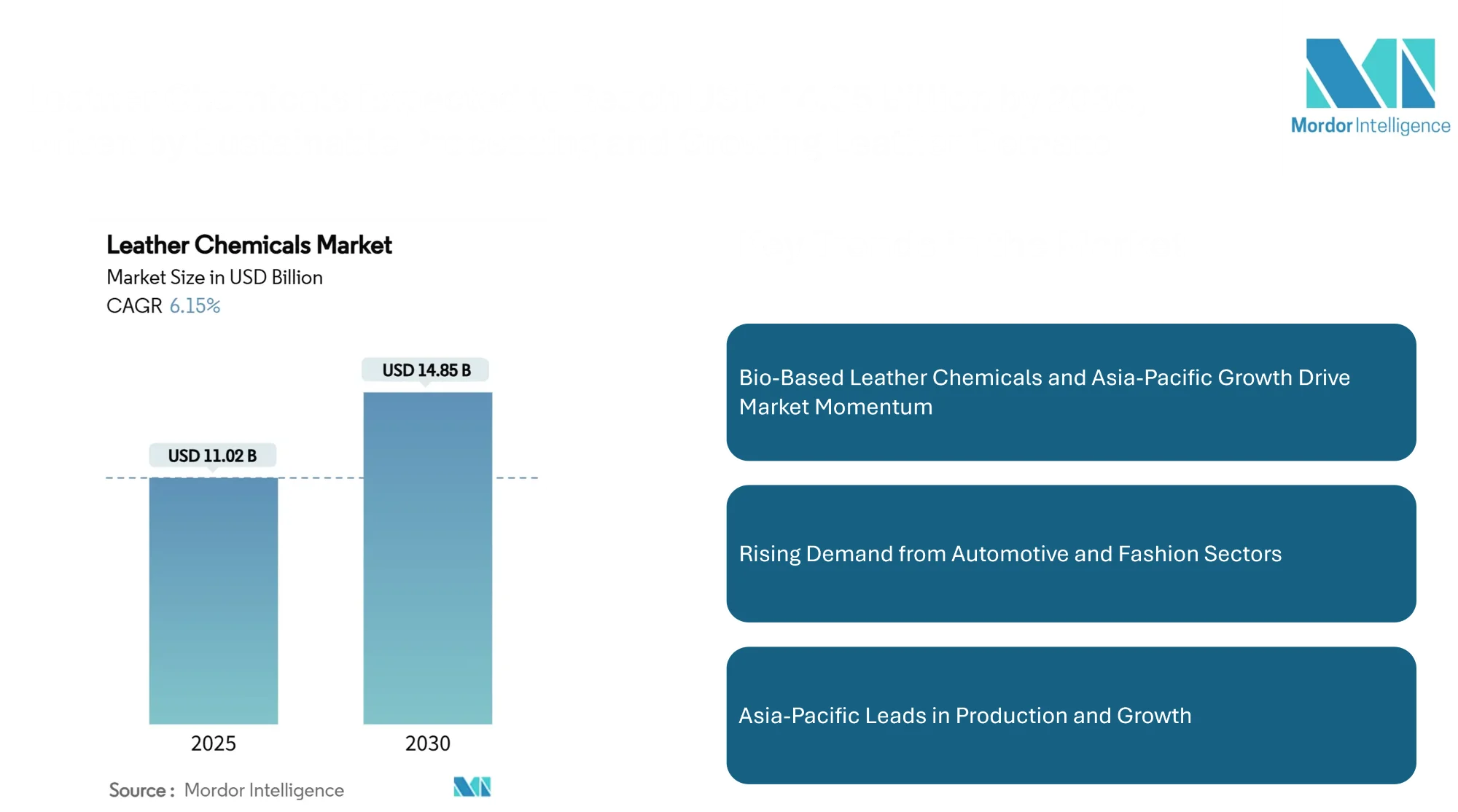

Global Leather Chemicals Market Size is projected to grow from USD 8.56 billion in 2024 to USD 11.15 billion by 2030, registering a CAGR of 4.46% during the forecast period, according to Mordor Intelligence. The industry is witnessing increased demand across multiple end-use sectors such as footwear, automotive, and fashion.

Leather chemicals are essential in processing raw hides into finished leather products, with applications ranging from tanning, beamhouse operations, and finishing. While the industry has traditionally relied on chromium and other synthetic agents, growing awareness around environmental sustainability is reshaping the product portfolio globally.

Report Overview: https://www.mordorintelligence.com/industry-reports/leather-chemicals-market?utm_source=globbook

Key Market Trends

Bio-Based and Chrome-Free Alternatives Are Gaining Traction

One of the strongest trends in the leather chemicals market is the move away from conventional heavy-metal-based agents, particularly chromium salts. Growing global concern over the environmental and health impacts of such agents has led to increased adoption of chrome-free and bio-based tanning agents. These alternatives support cleaner production processes and are better aligned with compliance requirements in developed markets.

Automotive and Fashion Sectors Bolstering Demand

The automotive industry, especially in luxury and mid-range segments, continues to drive demand for performance leather used in interiors. Similarly, the global fashion sector is witnessing a revival in leather usage, especially in handbags, shoes, and accessories, driving growth in finishing and dyeing chemicals.

Asia-Pacific Remains the Growth Hotspot

Countries like India, China, and Bangladesh continue to dominate leather manufacturing due to their abundant raw material supply, low labor costs, and export-oriented production bases. This has made Asia-Pacific the largest and fastest-growing region in the market, with ongoing investments in modernized tanneries and eco-friendly processing facilities further fueling expansion.

Check out more details and stay updated with the latest industry trends, including the Japanese version for localized insights: https://www.mordorintelligence.com/ja/industry-reports/leather-chemicals-market?utm_source=globbook

Market Segmentation

The leather chemicals market is segmented by product type, end-user industry, and geography:

By Product Type:

- Tanning & Dyeing Chemicals: Used in chrome tanning and alternative processes.

- Beamhouse Chemicals: Applied in soaking, liming, and dehairing operations.

- Finishing Chemicals: Used for improving leather aesthetics, feel, and performance.

By End-User Industry:

- Footwear and Leather Goods: Dominant segment due to high leather consumption.

- Automotive: Driven by demand for premium interiors.

- Furniture: Moderate but steady demand in luxury furniture production.

- Others: Includes industrial leather, saddlery, and sports equipment.

By Geography:

- Asia-Pacific: Largest and fastest-growing region with extensive manufacturing infrastructure.

- Europe: Focused on eco-compliance and premium leather production.

- North America: Moderate growth with increasing demand for chrome-free leather.

- Latin America, Middle East & Africa: Emerging manufacturing hubs and consumption regions.

Report Overview:

https://www.mordorintelligence.com/industry-reports/leather-chemicals-market?utm_source=globbook

Key Players

The global leather chemicals market is moderately consolidated, with a mix of multinational giants and regional suppliers. Key players are focusing on expanding sustainable product lines, enhancing R&D capabilities, and forming partnerships with tanneries to maintain competitiveness.

- LANXESS AG: A major supplier of leather tanning and finishing agents, with growing focus on sustainable products.

- Stahl Holdings BV: Offers a comprehensive portfolio of leather chemicals with a strong emphasis on environmental stewardship.

- TFL Ledertechnik GmbH: Known for its advanced beamhouse and dyeing solutions and consistent investment in cleaner technologies.

- Sisecam Chemicals: Supplies chemicals with a strong distribution network across regions.

- Zschimmer & Schwarz: Focuses on tailor-made specialty chemicals for leather finishing.

Other players include Zschimmer & Schwarz, Balmer Lawrie & Co. Ltd., Indofil Industries Limited, and DyStar Group, each contributing to regional or segment-specific growth in leather chemical applications.

Conclusion

The global leather chemicals market is evolving, marked by a clear transition toward sustainability, process efficiency, and regulatory compliance. While traditional segments like footwear and automotive interiors continue to drive volumes, growth is increasingly tied to environmental performance and product differentiation.