Introduction – Rising Demand for Natural Ingredients Fuels Global Pectin Market Expansion

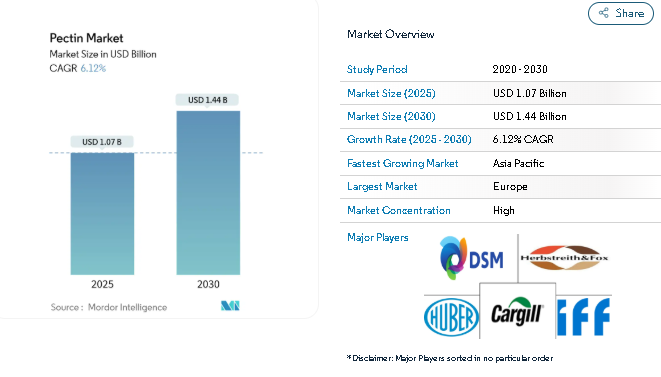

The Global Pectin Market is projected to grow from USD 1.07 billion in 2025 to USD 1.44 billion by 2030, registering a compound annual growth rate (CAGR) of 6.12%, according to the Pectin Market Industry Report by Mordor Intelligence.

This growth is propelled by increasing consumer demand for clean-label, plant-based, and functional ingredients, along with tightening regulations around artificial stabilizers and synthetic hydrocolloids.

As a natural polysaccharide extracted mainly from citrus fruits and apples, pectin has become a key ingredient across the food, beverage, pharmaceutical, and cosmetic industries. While Europe remains the largest market for pectin due to its strong sustainability focus, the Asia-Pacific region is rapidly emerging as a high-growth market driven by rising health awareness and the popularity of functional, pectin-based foods.

Key Trends – Clean-Label Movement and Functional Innovation Reshape Market Outlook

1. Clean-Label and Plant-Based Ingredient Revolution

The global transition toward natural and transparent food ingredients has significantly boosted demand for pectin. Food and beverage manufacturers are increasingly replacing synthetic stabilizers with pectin to meet consumer preferences for traceable, non-GMO, and plant-derived products.

Retailers across Europe and North America are emphasizing “free-from” and “natural” claims, encouraging producers to adopt sustainable sourcing and clean-label certifications. This transformation aligns with global regulatory support favoring plant-based food additives and bio-based polymers.

2. Growth of Packaged and Convenience Foods

With rapid urbanization and busier lifestyles, the consumption of ready-to-eat and shelf-stable foods is soaring. Pectin’s multifunctional properties—acting as a natural gelling agent, stabilizer, and thickener—make it essential for enhancing texture, consistency, and shelf life in products like dairy, sauces, and fruit preparations.

As global consumers demand convenient yet high-quality foods, pectin’s presence across processed food segments continues to strengthen.

3. Surge in Vegan and Gelatin-Free Confectionery

A key driver of pectin’s popularity is the shift toward vegan, halal, and plant-based confectionery. More than half of new gummy and jelly product launches now utilize pectin instead of gelatin, offering superior texture and compatibility with low-sugar formulations.

This trend underscores the pectin market’s role in addressing ethical, dietary, and sustainability concerns while expanding into functional confectionery designed for wellness-conscious consumers.

4. Expanding Applications in Pharmaceuticals and Biomedicine

Beyond food, pectin’s biocompatibility and gel-forming abilities are unlocking new opportunities in drug delivery systems, wound healing, nutraceuticals, and 3D bioprinting. Pectin hydrogels are increasingly used for controlled-release pharmaceuticals and bioadhesive materials, adding high-value potential to the pectin market industry landscape.

5. Supply Chain and Raw Material Challenges

Despite growing demand, the pectin industry faces raw material challenges. Citrus greening disease in Brazil has constrained citrus supplies, causing price volatility. In response, manufacturers are diversifying sources to include apple, sugar beet, and sunflower pectin to stabilize supply chains and reduce production risk.

Meanwhile, synthetic hydrocolloid substitutes like carboxymethyl cellulose continue to pose cost-based competition in developing markets.

Market Segmentation – Source, Type, Category, Application, and Regional Insights

By Source

-

Citrus Fruits remain the dominant source due to superior gelling quality and availability in major producing regions.

-

Apple Pectin is rapidly growing in popularity, supported by sustainable extraction advancements.

-

Alternative Sources like sugar beet and sunflower pectin are emerging as viable options for reducing dependency on citrus crops.

By Type

-

High-Methoxyl Pectin (HMP) leads the market, widely used in jams, jellies, and high-sugar bakery fillings.

-

Low-Methoxyl Pectin (LMP) is gaining traction for low-sugar, calcium-induced formulations aligned with diabetic and health-conscious product lines.

By Category

-

Conventional Pectin dominates due to cost efficiency and established manufacturing infrastructure.

-

Organic Pectin is the fastest-growing segment, driven by consumer demand for organic-certified, eco-friendly, and non-GMO ingredients.

By Application

-

Food and Beverage applications account for the largest market share, spanning jams, dairy, beverages, and desserts.

-

Pharmaceuticals and Nutraceuticals are rapidly emerging segments using pectin in drug encapsulation and supplement coatings.

-

Cosmetics and Personal Care industries are also incorporating pectin for skin-friendly formulations and natural emulsifiers.

By Region

-

Europe leads global consumption, underpinned by clean-label consumer behavior and robust citrus processing industries.

-

Asia-Pacific is the fastest-growing market, with countries like China and India adopting natural food additives and expanding local manufacturing.

-

North America shows steady growth, supported by innovation in functional foods and dietary supplements.

-

South America, the Middle East, and Africa represent emerging opportunities driven by increasing awareness of plant-based and sustainable ingredients.

Key Players – Strategic Expansion and Sustainable Innovation

The global pectin market remains moderately consolidated, with top players focusing on M&A activities, capacity expansion, and sustainable extraction technologies.

In 2024, Tate & Lyle’s acquisition of CP Kelco for USD 1.8 billion significantly reshaped the hydrocolloids sector, combining two industry leaders in natural stabilizers.

Other major players include:

-

Cargill Incorporated

-

International Flavors & Fragrances (IFF)

-

Herbstreith & Fox Corporate Group

-

Silvateam S.p.A.

-

Ingredion Incorporated

Leading companies are investing in R&D to develop next-generation pectin products, such as IFF’s Grindsted Pectin FB 420 for bakery applications and Cargill’s expansion of regional pectin production in Asia.

Smaller, regional firms are differentiating through organic certifications, local sourcing, and traceability systems targeting eco-conscious brands.

Conclusion – Sustainable Growth Path for the Global Pectin Market

The Global Pectin Market Outlook (2025–2030) highlights a strong growth trajectory anchored in clean-label innovation, plant-based product expansion, and sustainability-driven sourcing.

Despite short-term constraints from raw material shortages and synthetic alternatives, the industry’s long-term fundamentals remain robust, supported by advancements in extraction efficiency and diversified raw material utilization.

As consumers and regulators increasingly prioritize health transparency, natural formulations, and environmental responsibility, pectin stands out as a cornerstone ingredient for the next generation of food, pharmaceutical, and wellness innovations.

Manufacturers embracing sustainable production and value-added product development are poised to capture substantial market share in this evolving, high-potential sector.