Introduction to the Asia-Pacific Dog Food Market

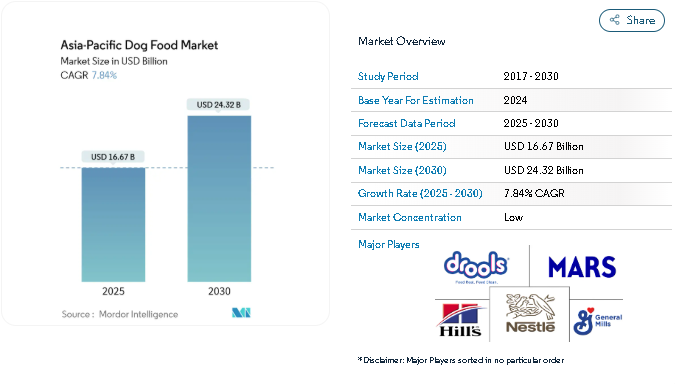

The Asia-Pacific dog food market is entering a strong growth phase as pet owners across the region continue to spend more on nutrition, wellness, and tailored feeding solutions for their dogs. Valued at USD 16.67 billion in 2025, the market is projected to hit USD 24.32 billion by 2030, reflecting a 7.84% CAGR during the forecast period.

The rise of pet humanization, expanding middle-class incomes, and increasing access to online and specialty outlets are reshaping buying patterns across countries like China, Australia, Japan, India, South Korea, Thailand, Indonesia, and Malaysia. Consumers are making more informed decisions about ingredients, digestibility, breed suitability, and veterinary-recommended diets. As a result, brands offering natural ingredients, convenient formats, and health-focused formulations are seeing faster adoption.

Growing attention to pet health is also boosting demand for veterinary diets, functional formulas, and supplements. At the same time, domestic manufacturers continue to compete with global brands by offering localized recipes and price-flexible options suited to diverse markets in the region.

Key Trends in the Asia-Pacific Dog Food Market

Premium and Human-Grade Ingredients Gain Strong Preference

One of the most visible shifts in the Asia-Pacific dog food market is the rising preference for products made with fresh meat, limited additives, and recognizable ingredients. Pet owners in China, Japan, Australia, and Southeast Asian countries are increasingly choosing recipes that reflect household food standards.

Brands are emphasizing clean ingredients, shorter labels, and transparent sourcing. Fresh-meat-first formulas, grain-free options, and recipes without artificial flavors or preservatives are gaining traction. Many shoppers also look for allergen-friendly options or diets catering to digestive sensitivity, skin health, and joint support.

Human-grade and sustainable ingredient sourcing has started to influence purchasing behavior, especially in urban areas. Certifications related to food safety and production quality—such as HACCP and ISO 22000—add confidence and strengthen brand trust among premium buyers.

Online-to-Offline Retail Integration Redefines Access

Digital retail continues to reshape the Asia-Pacific dog food market, especially in countries where e-commerce adoption is far ahead of global averages. In China, online platforms account for nearly half of total dog food sales, with brand-owned flagship stores becoming a major channel.

Platforms across South Asia and Southeast Asia—such as Shopee, Lazada, Flipkart, and TikTok Shop—allow both global and domestic brands to reach consumers quickly. Subscription-based deliveries, bundled offers, and personalized recommendations have become part of the regional retail ecosystem.

Veterinary practices and specialty pet stores are also moving toward hybrid models. These O2O approaches integrate medical advice, product consultation, and digital ordering, offering convenience while maintaining expert oversight.

Rapid Growth in Urban Dog Ownership

Increasing disposable income, smaller household sizes, and shifting lifestyle patterns contribute to steady growth in pet ownership in the region. Countries such as China, the Philippines, Vietnam, Thailand, and India report rising pet adoption rates, with dogs remaining the most popular companion animal.

Urban pet owners spend more on nutrition and diet-specific food formats that support long-term health. Many cities also have better access to premium pet stores, veterinary clinics, and grooming centers, further encouraging structured feeding practices.

Functional and Breed-Specific Diets Strengthen Market Depth

The demand for functional dog food is increasing, particularly diets designed to address skin issues, weight management, joint mobility, digestive health, or breed-specific needs. Veterinary clinics often recommend specialized formulas, giving this category a steady growth path.

Insect-based proteins, limited-ingredient diets, and hypoallergenic recipes are emerging in select markets, though regulations vary across Asia-Pacific. As pet owners become more aware of targeted nutrition, they increasingly combine regular diets with supplements rich in omega-3, probiotics, or glucosamine.

Raw Material Price Swings Influence Product Pricing

The dog food industry in Asia-Pacific is sensitive to changes in meat and animal fat prices. Weather disruptions, global freight fluctuations, and disease outbreaks often influence ingredient availability. Some manufacturers balance these challenges through long-term sourcing contracts, regional ingredient partnerships, and alternative protein options.

Market Segmentation in the Asia-Pacific Dog Food Market

By Pet Food Product

-

Food (Dry and Wet Dog Food) – Dry kibble dominates due to affordability, storage convenience, and suitability for daily feeding.

-

Pet Treats – Includes crunchy treats, dental chews, soft-chewy sticks, jerky, and freeze-dried formats.

-

Pet Nutraceuticals/Supplements – Vitamins, probiotics, omega-3 oils, proteins, and functional blends for preventive health.

-

Veterinary Diets – Formulas designed for conditions such as digestive sensitivity, renal issues, diabetes, or obesity.

Key points:

-

Dry food maintains the largest share of the category.

-

Wet food and air-dried formats attract senior dogs and picky eaters.

-

Supplements are growing fastest in Japan, Australia, and South Korea.

-

Veterinary diets continue to expand in urban markets.

By Distribution Channel

-

Specialty Stores – Lead in premium and therapeutic diets due to expert guidance.

-

Online Channels – Offer the widest variety and strong discounts.

-

Convenience Stores – Growing quickly in high-density markets with extended operating hours.

-

Supermarkets/Hypermarkets – Popular for mid-range household brands.

-

Other Channels – Includes veterinary clinics, pet service outlets, and traditional shops in emerging markets.

Key Players in the Asia-Pacific Dog Food Market

The competitive landscape includes global leaders and increasingly strong domestic brands. Key companies operating in the Asia-Pacific dog food market include:

-

Mars Incorporated

-

Nestlé Purina

-

General Mills Inc.

-

Hill’s Pet Nutrition (Colgate-Palmolive)

-

Drools Pet Food Pvt. Ltd.

These companies maintain a strong presence through diversified portfolios, research collaborations, and regional manufacturing facilities. Local brands across China, Thailand, Malaysia, Indonesia, and India continue to gain ground by introducing cost-effective products and recipes adapted to local taste preferences.

Conclusion

The Asia-Pacific dog food market is on a solid upward path, supported by rising pet ownership, growing interest in high-quality nutrition, and expanding access to digital shopping. Premium diets, natural ingredients, and functional formulations are becoming common in both developed and developing markets across the region.

As consumers continue to prioritize their pets’ well-being, the industry is expected to expand across all major segments—dry food, wet food, treats, supplements, and veterinary diets. With strong growth forecasts and increasing competition, Asia-Pacific remains one of the most attractive regions for global and local dog food brands through 2030.

About Mordor Intelligence:

Mordor Intelligence is a trusted partner for businesses seeking comprehensive and actionable market intelligence. Our global reach, expert team, and tailored solutions empower organizations and individuals to make informed decisions, navigate complex markets, and achieve their strategic goals.

With a team of over 550 domain experts and on-ground specialists spanning 150+ countries, Mordor Intelligence possesses a unique understanding of the global business landscape. This expertise translates into comprehensive syndicated and custom research reports covering a wide spectrum of industries, including aerospace & defense, agriculture, animal nutrition and wellness, automation, automotive, chemicals & materials, consumer goods & services, electronics, energy & power, financial services, food & beverages, healthcare, hospitality & tourism, information & communications technology, investment opportunities, and logistics.