Introduction: Fitness Equipment Market Outlook (2025–2030)

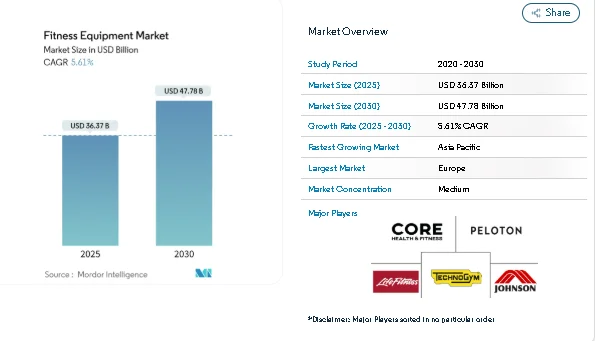

The global fitness equipment market is entering a steady growth phase as consumers shift toward healthier routines, structured exercise programs, and data-supported training experiences. According to current assessments, the market is valued at USD 36.37 billion in 2025 and is expected to reach USD 47.78 billion by 2030, recording a 5.61% CAGR.

Growing awareness around lifestyle-related health risks, rising obesity levels, and a clear preference for personalized workout plans have widened the consumer base for both home and commercial fitness equipment. Manufacturers are strengthening product lines with digital features, compact designs, and user-friendly interfaces that support long-term fitness engagement.

At the same time, fitness centers, sports clubs, hospitals, and corporate wellness programs continue to refresh and expand their equipment inventory, keeping commercial demand stable.

Key Trends Driving the Fitness Equipment Market

1. Higher Focus on Healthy Living and Preventive Wellness

Fitness has transitioned from a hobby to an essential part of everyday life. People across age groups are prioritizing simple, consistent workout routines that help manage weight, stress, and chronic conditions. This shift is boosting demand for treadmills, stationary bikes, strength systems, and multi-functional home gyms.

Interest in wearable technology and workout tracking apps has also grown. While these tools support outdoor and indoor activities, they often sync directly with modern equipment, creating a seamless training experience. Younger consumers, in particular, view fitness gear as a long-term household investment rather than a luxury purchase.

2. Growing Prevalence of Obesity and Lifestyle Diseases

Global obesity levels have increased sharply over the past decade, contributing to higher cases of diabetes, hypertension, and heart-related disorders. As structured exercise becomes a part of medical recommendations, fitness equipment is increasingly used in rehabilitation centers, physiotherapy settings, and home-based recovery routines.

Governments and healthcare organizations are encouraging physical activity to ease long-term healthcare costs. This adds steady momentum to the market, supporting both affordable mass-market equipment and premium systems designed for focused workout goals.

3. Rise of Smart and Connected Fitness Equipment

Smart fitness equipment is gaining acceptance among users seeking guided workouts, real-time feedback, and customized training plans. Touchscreen dashboards, workout history tracking, integrated sensors, and app connectivity are becoming standard in newer models.

Brands offering systems with guided form correction, resistance control, movement tracking, and interactive training experiences are drawing interest from gyms and home-fitness adopters. This trend is reshaping product preferences, especially in markets with strong digital adoption.

4. Home Fitness Becomes a Long-Term Habit

Home-based workouts remain popular due to convenience, privacy, and time savings. Compact treadmills, foldable bikes, functional trainers, and all-in-one strength machines are gaining traction. Families are investing in equipment that supports multiple workout styles and user profiles.

Modern designs also cater to urban homes with limited space, further expanding demand for small-footprint yet durable machines.

Market Segmentation: Fitness Equipment Market Breakdown

By Product Type

The market includes:

-

Treadmills

-

Elliptical machines

-

Stationary cycles

-

Rowing machines

-

Strength training equipment

-

Other equipment types

Treadmills remain the leading category due to familiar usage and wide applicability—from basic walking routines to advanced running sessions.

Strength training equipment is the fastest-growing category as consumers shift toward muscle-building, rehabilitation, and functional fitness routines.

By Category

-

Conventional equipment

-

Smart/connected equipment

Conventional machines continue to dominate due to reliability and lower maintenance needs. Smart equipment, however, is expanding quickly as tech-savvy users seek workout guidance, digital tracking, and integrated coaching.

By End Use

-

Commercial

-

Residential

Commercial facilities—including gyms, corporate centers, and sports training institutes—hold the largest share. Residential use is growing rapidly as home gyms become mainstream and consumers aim for flexible schedules.

By Price Range

-

Mass market

-

Premium

The mass segment attracts budget-sensitive buyers looking for essential features. The premium segment is accelerating faster, supported by higher-income consumers who seek advanced features, superior build quality, and digital integration.

By Distribution Channel

-

Offline channels

-

Online channels

Offline stores remain dominant due to the need for physical product evaluation and installation support. Online platforms are gaining momentum through better product visualization, demos, customer reviews, and direct-to-consumer brand strategies.

Key Players in the Fitness Equipment Market

The fitness equipment industry is moderately consolidated with global and regional brands competing through product quality, durability, digital features, and after-sales services. Major companies include:

-

Technogym S.p.A.

-

Johnson Health Tech Co. Ltd.

-

Life Fitness LLC

-

Core Health & Fitness LLC

-

Peloton Interactive Inc.

These companies maintain strong distribution networks and develop equipment for both home and commercial use. Many are expanding their ecosystem approaches—combining hardware with digital training content, subscription-based workout programs, and connected platforms.

Smaller brands and niche manufacturers are also finding opportunities, particularly in compact equipment, affordable home gym systems, and region-specific product lines.

Conclusion: Fitness Equipment Market Outlook to 2030

The global fitness equipment market is set for steady expansion as consumers, healthcare providers, and commercial fitness facilities continue to adopt structured physical activity. Rising awareness of healthy living, an aging population, and demand for smart workout options will keep fueling market growth.

While conventional equipment still holds the majority share, connected machines and digital workout ecosystems are shaping future purchase patterns. Manufacturers focusing on affordability, durability, user comfort, and integrated digital features will be well-positioned in the years ahead.

By 2030, the market is expected to reach USD 47.78 billion, reflecting a long-term consumer shift toward preventive healthcare and accessible fitness solutions.

About Mordor Intelligence:

Mordor Intelligence is a trusted partner for businesses seeking comprehensive and actionable market intelligence. Our global reach, expert team, and tailored solutions empower organizations and individuals to make informed decisions, navigate complex markets, and achieve their strategic goals.

With a team of over 550 domain experts and on-ground specialists spanning 150+ countries, Mordor Intelligence possesses a unique understanding of the global business landscape. This expertise translates into comprehensive syndicated and custom research reports covering a wide spectrum of industries, including aerospace & defense, agriculture, animal nutrition and wellness, automation, automotive, chemicals & materials, consumer goods & services, electronics, energy & power, financial services, food & beverages, healthcare, hospitality & tourism, information & communications technology, investment opportunities, and logistics.