Introduction

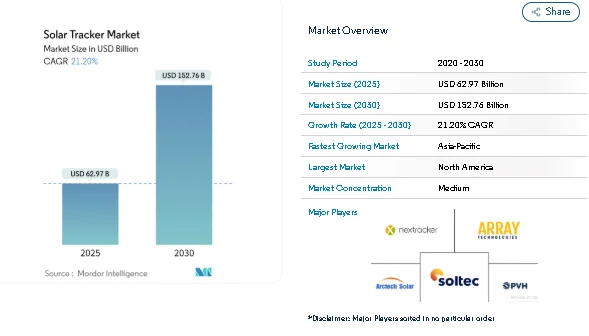

The solar tracker industry is poised for strong expansion over the next few years. The global solar tracker market, valued at USD 62.97 billion in 2025, is projected to reach USD 152.76 billion by 2030, registering a 21.2% CAGR. This growth is driven by rising demand for higher energy yield, supportive renewable-energy policies, and declining solar technology costs. Increasing adoption of tracker-equipped utility-scale projects further reinforces the market’s role as a critical component of global solar deployment.

Market Drivers & Insights in the Solar Tracker Market

Rising Utility-Scale Deployments and Policy Support

A major driver of solar tracker adoption is the growing volume of utility-scale solar projects. Lower costs for solar panels combined with supportive policies and incentives in various regions make trackers an attractive way to boost energy yield.

Cost Pressure Drives Design Innovation

Despite increasing demand, tracker manufacturers face margin pressure due to rising steel prices and supply-chain constraints. To counter this, the industry is moving toward lighter structures, such as single-post frames and modular designs, which reduce raw material usage and simplify installation.

Technological Segmentation: From Photovoltaic to Concentrated Photovoltaic

The solar tracker market remains dominated by photovoltaic (PV) modules, which held around 85% share in 2024. That dominance is underlined by widespread global PV manufacturing and mature procurement frameworks.

Access the complete data-driven outlook on the solar tracker market now - https://www.mordorintelligence.com/industry-reports/solar-tracker-market?utm_source=globbook

Market Breakdown

By Axis Type

-

Single-Axis: Holds the largest share — about 53% in 2024. These systems offer a balance of improved energy yield and manageable cost, which makes them a preferred option for many utility-scale and large-ground-mounted projects.

-

Dual-Axis: While still a smaller share today, dual-axis trackers are gaining traction, particularly for specialized projects in high-latitude or land-constrained areas. Their growth trajectory is steeper, reflecting demand for higher energy yield per unit area.

By Technology

-

Photovoltaic (PV): The backbone of the tracker market with 85% market share in 2024.

-

Concentrated Photovoltaic (CPV): Growing rapidly, with rising interest in CPV-plus-tracker combinations, especially in regions with strong direct sunlight and optimal land conditions.

By Application

-

Utility-Scale Projects: Nearly 82% of tracker deployments as of 2024 — developers of large solar farms continue to dominate demand.

-

Commercial & Industrial (C&I): Growing at a fast rate; as corporations adopt renewable power targets and behind-the-meter solar becomes profitable, tracker installations on C&I sites are rising.

-

Other / Emerging Uses: Smaller-scale or non-traditional applications (e.g., micro-grids, remote installations) where lighter or modular trackers may be beneficial, especially when paired with storage or hybrid systems.

By Drive Type

-

Electric Motor Drives: Dominated the market in 2024 (about 78% share), valued for precise motion control and low field maintenance, making them suitable for large installations.

-

Hydraulic & Linear Actuators: Rising in popularity, particularly in environments demanding higher torque, sturdiness, or precision. Growth in these segments reflects adaptation to varied site conditions and climates.

For a more tailored understanding, view the localized Japanese edition alongside the global market breakdown - https://www.mordorintelligence.com/ja/industry-reports/solar-tracker-market?utm_source=globbook

-

Leading Companies in the Solar Tracker Market

-

Nextracker leads in global shipments and has recently strengthened its foothold by integrating foundation and power-electronics capabilities through strategic acquisitions.

-

Array Technologies continues to emphasize mechanical simplicity and cost-efficiency, appealing to projects where minimizing material and maintenance costs is critical.

-

Arctech Solar leverages its global manufacturing footprint — especially in regions like Central Asia and the Middle East — to serve markets with competitive price and delivery pressures.

-

Other firms — including PV Hardware, GameChange Solar, and Soltec Power Holdings — address price-sensitive markets through regional manufacturing and tailored delivery models, often focusing on volume and local compliance rather than premium features.

Conclusion

The global solar tracker market is on track to more than double by 2030, in large part because of falling solar panel costs, supportive policies, and increased adoption of utility-scale solar. For stakeholders in solar energy — from project developers to components suppliers — the coming years are likely to see a wave of growth centered around solar trackers, making this segment a key building block for the transition to cleaner, more efficient solar power worldwide.

About Mordor Intelligence:

With a team of over 550 domain experts and on-ground specialists spanning 150+ countries, Mordor Intelligence possesses a unique understanding of the global business landscape. This expertise translates into comprehensive syndicated and custom research reports covering a wide spectrum of industries, including aerospace & defense, agriculture, animal nutrition and wellness, automation, automotive, chemicals & materials, consumer goods & services, electronics, energy & power, financial services, food & beverages, healthcare, hospitality & tourism, information & communications technology, investment opportunities, and logistics.

For any inquiries, please contact: