Introduction: Sports Drinks Market Overview

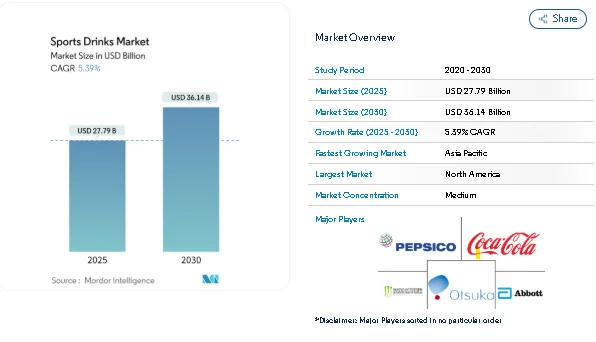

The global sports drinks market, valued at USD 27.79 billion in 2025, is projected to reach USD 36.14 billion by 2030, growing at a CAGR of 5.39%. The market has evolved beyond professional athletes, now catering to a wider consumer base focused on everyday wellness. Increasing fitness club memberships, urbanization, and higher disposable incomes—especially in the Asia-Pacific region—are fueling demand for convenient, functional hydration solutions. Health-conscious consumers are also gravitating toward products with reduced sugar content, clean-label ingredients, and environmentally sustainable packaging. With global event sponsorships and corporate wellness programs boosting visibility, sports drinks have become a staple not just for athletes but for anyone engaged in regular physical activity.

Key Trends in the Sports Drinks Market

Rising Participation in Physical Activities

Fitness participation is steadily increasing worldwide, particularly among younger populations in the Asia-Pacific region. Partnerships between major brands and fitness chains, such as Gatorade’s collaboration with Anytime Fitness Philippines and Red Bull’s tie-up with F45 Training Australia, reflect the shift from occasional sports consumption to routine hydration during workouts. In the U.S., 78.8% of adults engaged in physical activity in 2023, highlighting the growing potential for market expansion beyond traditional athletic demographics.

Demand for Targeted Hydration and Electrolyte Replenishment

Consumer interest in electrolyte-balanced formulations is growing, with products now catering to daily hydration needs rather than only high-intensity athletic performance. Examples include Gatorade’s Hydration Booster, which focuses on electrolyte replenishment for general wellness. This trend emphasizes the importance of scientific credibility in marketing, moving beyond athlete endorsements to connect with a broader audience.

Expansion of Distribution Channels

The sports drinks market is benefiting from diversified distribution channels, including convenience stores, specialty fitness retailers, and online platforms. Off-trade channels, like supermarkets and convenience stores, dominate due to their accessibility, while online retail is strengthening direct-to-consumer engagement. Brands such as Liquid I.V. are leveraging e-commerce to offer personalized hydration solutions and subscription models.

Sugar-Free and Low-Calorie Options

Health-conscious consumers are increasingly seeking sugar-free or low-calorie alternatives without compromising on taste or effectiveness. Coca-Cola’s BodyArmor Zero Sugar, which uses natural sweeteners like stevia and monk fruit, addresses this demand. Additionally, the inclusion of functional ingredients such as amino acids, vitamins, and adaptogens is shaping premium offerings, creating new opportunities for differentiation in the market.

Regulatory and Shelf-Life Considerations

Natural and preservative-free sports drinks face challenges with stability and shelf life, particularly in regions with variable climates. Advances in aseptic packaging and PET bottle technology help extend product longevity without chemical preservatives, allowing brands to meet consumer demand for cleaner formulations. Regulatory compliance remains critical, especially for products bordering dietary supplement claims, which may affect launch timelines and marketing strategies.

Market Segmentation

The sports drinks market is segmented by type, packaging, distribution, functionality, and geography:

By Soft Drink Type:

-

Isotonic: Dominates with 53.12% market share in 2024, matching human plasma osmolality for efficient hydration.

-

Hypertonic: Fastest-growing segment at a 6.74% CAGR, ideal for intense endurance activities.

-

Hypotonic: Offers rapid hydration during moderate exercise.

-

Electrolyte-Enhanced Water: Targets wellness-focused consumers seeking functional hydration.

-

Protein-Based Drinks: Supports muscle recovery post-workout.

By Packaging Type:

-

PET Bottles – 57.09% market share

-

Aseptic Packages – Fastest-growing with 6.91% CAGR

-

Glass Bottles – Premium positioning

-

Metal Cans – Recyclable and thermally efficient

By Distribution Channel:

-

Off-Trade (Supermarkets, Convenience Stores) – 63.93% share

-

On-Trade (Gyms, Cafes, Fitness Centers) – 6.83% CAGR

By Functionality:

-

Post-Workout – 48.23% share, focusing on muscle recovery

-

Intra-Workout – 6.71% CAGR, for hydration during exercise

-

Pre-Workout – Enhances energy and performance

By Geography:

-

North America: Largest market with 38.11% share in 2024

-

Asia-Pacific: Fastest-growing region with 6.33% CAGR, led by China, Japan, and South Korea

-

Europe, Middle East & Africa, and South America present steady growth opportunities with increasing urbanization and fitness adoption.

Key Players in the Sports Drinks Market

The market features a mix of multinational corporations and emerging niche brands. Major players include:

-

PepsiCo, Inc. – Offers Gatorade and related hydration products.

-

The Coca-Cola Company – Markets BodyArmor and Powerade, including zero-sugar options.

-

Otsuka Holdings Co., Ltd. – Focuses on functional sports beverages.

-

Monster Beverage Corporation – Combines energy and sports drinks to capture younger demographics.

-

Abbott Laboratories – Develops nutrition-focused sports drinks with functional benefits.

These companies leverage strong distribution networks, brand recognition, and partnerships with fitness providers to maintain market share while also exploring premium and functional product offerings.

Conclusion: Sports Drinks Market Outlook

The global sports drinks market is set for steady growth through 2030, driven by broader consumer adoption, increased health awareness, and innovation in functional formulations. While isotonic beverages continue to dominate, hypertonic and intra-workout solutions are gaining traction. Off-trade channels remain the primary revenue driver, but e-commerce and specialty retail are increasingly influential. Health-conscious trends, including sugar-free options and natural ingredient formulations, are shaping the market’s future. With Asia-Pacific emerging as the fastest-growing region and established players strengthening their presence globally, the sports drinks market is positioned to cater to diverse hydration needs, from casual fitness enthusiasts to dedicated athletes.

About Mordor Intelligence:

Mordor Intelligence is a trusted partner for businesses seeking comprehensive and actionable market intelligence. Our global reach, expert team, and tailored solutions empower organizations and individuals to make informed decisions, navigate complex markets, and achieve their strategic goals. With a team of over 550 domain experts and on-ground specialists spanning 150+ countries, Mordor Intelligence possesses a unique understanding of the global business landscape. This expertise translates into comprehensive syndicated and custom research reports covering a wide spectrum of industries, including aerospace & defense, agriculture, animal nutrition and wellness, automation, automotive, chemicals & materials, consumer goods & services, electronics, energy & power, financial services, food & beverages, healthcare, hospitality & tourism, information & communications technology, investment opportunities, and logistics.