Introduction: Agricultural Robots Market Overview

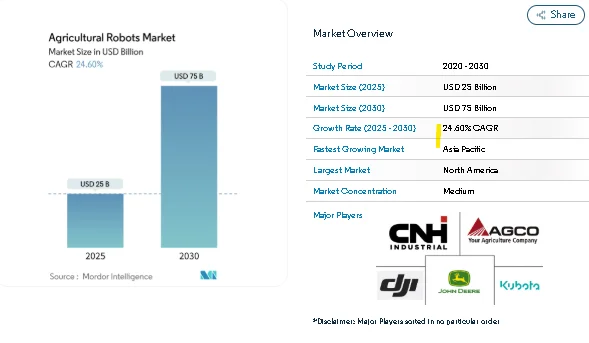

The agricultural robots market in the United States is set for significant growth, rising from USD 25 billion in 2025 to an estimated USD 75 billion by 2030, reflecting a strong compound annual growth rate (CAGR) of 24.6%. This rapid expansion is fueled by farmers’ increasing need to address labor shortages, boost crop yields, and reduce input waste. Autonomous machines equipped with artificial intelligence (AI), computer vision, and precision sensors are becoming integral to modern farming practices.

Flexible, high-performance agricultural robots are now capable of operating day and night across diverse crop types. Falling prices for sensors, cameras, and other components have made once high-cost technologies accessible to mid-sized and even smaller farms. While hardware continues to generate the largest share of revenue, software solutions and service agreements are gaining traction, offering predictive maintenance, data management, and integrated farm coordination. Government subsidies and incentives further support adoption by offsetting upfront costs and ensuring regulatory compliance for autonomous systems.

Key Trends Shaping the Agricultural Robots Market

1. Labor Shortages and Aging Farmer Population

The scarcity of skilled labor is a persistent challenge in U.S. agriculture. With many experienced workers retiring and younger generations seeking opportunities outside farming, farms face operational delays. Reports indicate that 60% of agribusinesses postponed projects in 2024 due to the inability to secure seasonal labor. Agricultural robots provide a continuous, reliable workforce capable of operating around the clock without overtime costs, helping growers maintain consistent field operations and reduce wage pressures.

2. Increased Venture and Corporate Investments

Investment in farm robotics continues to grow, even as general AgTech funding experiences fluctuations. In 2024, funding for robotic farming solutions rose 9%, signaling strong investor confidence. Collaborations such as New Holland with Bluewhite for retrofitting specialty tractors are expected to reduce operating costs by up to 85% for orchard and vineyard owners. Start-ups like Verdant Robotics and Fieldwork Robotics have secured multi-million-dollar investments, accelerating development and global launches. This investment influx keeps the agricultural robots market competitive and innovation-driven.

3. Government Support and Incentives

Public programs targeting sustainable farming practices encourage the adoption of autonomous technologies. For instance, the United Kingdom’s Improving Farm Productivity grant subsidizes part of the cost of robotic systems that integrate navigation, sensing, and analytics. In Australia, the National Robotics Strategy estimates robotics could contribute AUD 600 billion (USD 420 billion) to GDP, with agriculture identified as a priority sector. Such policies shorten payback periods and make advanced robotics feasible for small- and medium-sized farms.

4. Advances in AI, Computer Vision, and LIDAR

Modern agricultural robots leverage camera arrays, edge processors, and LIDAR technology to detect obstacles, classify plants, and optimize operations in real time. John Deere’s second-generation autonomy stack, for example, uses 16 cameras to provide centimeter-level precision under challenging conditions such as dust or fog. Similar sensor systems are applied in research harvesters for greenhouses, enabling fully autonomous operations in high-value horticulture crops.

Market Segmentation: Agricultural Robots Market Insights

By Type:

-

Unmanned Aerial Vehicles (Drones): Hold 35% market share, widely used for aerial imaging, spraying, and crop monitoring.

-

Automated Harvesters: Fastest-growing segment with a 26% CAGR, addressing labor shortages in fruit and vegetable harvesting.

-

Driverless Tractors: Growing at 27% CAGR as fleets are retrofitted for autonomous field operations.

By Application:

-

Broad-Acre Farming: Largest share (24% in 2024), involving mapping, fertilization, and inter-row weeding.

-

Greenhouse Automation: Growing at 24% CAGR, driven by high-value crops and controlled environment farming.

-

Dairy Farm Management: Focused on milking automation and herd monitoring.

-

Aerial Data Collection: Drones collecting precision data for crop stress detection and yield optimization.

By Offering:

-

Hardware: Dominates 60% of revenue, including robotic arms, chassis, and navigation systems.

-

Software: Fastest-growing at 21% CAGR, covering farm management platforms, fleet coordination, and cloud dashboards.

-

Services: Maintenance, training, and subscription-based support programs for robot fleets.

By Geography:

-

North America: Leading market (37% revenue share), supported by large farms, VC funding, and supportive regulations.

-

Asia-Pacific: Fastest-growing region at 25.5% CAGR, led by China, Japan, and Australia through subsidies and domestic innovation.

-

Europe: Steady growth due to labor shortages, sustainability policies, and high crop protection standards.

Key Players in the Agricultural Robots Market

The market is moderately concentrated, with leading suppliers capturing 56% of global revenue. Major players include:

-

John Deere: Leader in autonomous tractors and AI-powered field solutions.

-

CNH Industrial: Offers retrofitted autonomy kits and fleet solutions.

-

AGCO Corporation: Provides OutRun retrofit kits and precision farming equipment.

-

Kubota Corporation: Focused on driverless tractors and crop-specific robotics.

-

SZ DJI Technology Co., Ltd.: Global drone leader for agricultural imaging and spraying solutions.

Smaller players and start-ups address niche requirements, such as selective harvesting, chemical-free weeding, and smallholder-friendly automation, keeping competition high and fostering innovation.

Conclusion: Agricultural Robots Market Outlook

The U.S. agricultural robots market is entering a period of rapid growth driven by labor shortages, AI and sensor technology, and supportive policies. Broad-acre farming, greenhouse automation, and precision dairy management are key areas of adoption. While upfront costs and regulatory variation remain challenges, hardware, software, and services together are creating integrated farm solutions. With continued investment from corporates and venture funds, the agricultural robots market is poised to expand significantly, helping farms become more efficient, sustainable, and resilient through 2030.

About Mordor Intelligence:

Mordor Intelligence is a trusted partner for businesses seeking comprehensive and actionable market intelligence. Our global reach, expert team, and tailored solutions empower organizations and individuals to make informed decisions, navigate complex markets, and achieve their strategic goals.

With a team of over 550 domain experts and on-ground specialists spanning 150+ countries, Mordor Intelligence possesses a unique understanding of the global business landscape. This expertise translates into comprehensive syndicated and custom research reports covering a wide spectrum of industries, including aerospace & defense, agriculture, animal nutrition and wellness, automation, automotive, chemicals & materials, consumer goods & services, electronics, energy & power, financial services, food & beverages, healthcare, hospitality & tourism, information & communications technology, investment opportunities, and logistics.