Introduction: Expanding Role of Agriculture Drones

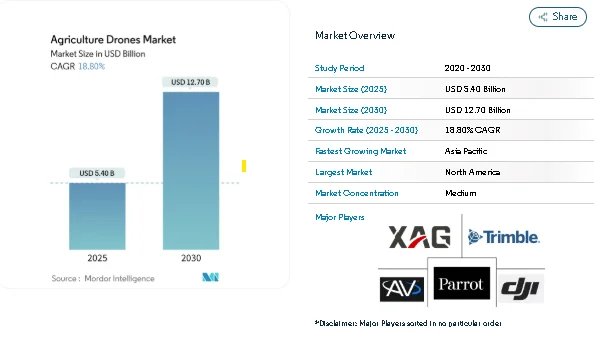

The global agriculture drones market is set for remarkable growth, with an estimated value of USD 5.40 billion in 2025, expected to reach USD 12.70 billion by 2030 at a CAGR of 18.8%. These drones are increasingly used in precision farming, field mapping, crop monitoring, and input applications, helping farmers improve productivity while reducing operational costs. Regulatory reforms in the United States and European Union have streamlined drone certification, allowing commercial spraying and monitoring operations to scale faster. Meanwhile, large-scale deployments in countries such as China and India demonstrate a clear transition from small pilot trials to full operational use, signaling strong adoption potential worldwide.

Hardware remains the main contributor to market revenue, yet software solutions are gaining traction by offering advanced analytics, automated insights, and variable-rate application planning. Medium-sized drones are becoming popular due to their larger payload capacities and extended flight times. Additionally, government initiatives promoting sustainable farming and carbon-smart practices are creating new revenue opportunities by monetizing data collected by these drones.

Key Trends Driving Agriculture Drones Market Growth

Precision Agriculture Adoption

The rise of precision farming has been a key factor driving the agriculture drones market. Variable-rate application techniques reduce herbicide usage by up to 25% and can increase farm income by USD 45–60 per hectare. Technologies such as real-time kinematic (RTK) positioning allow drones to apply inputs with centimeter-level accuracy, improving efficiency on irregularly shaped plots where traditional ground equipment may underperform. Globally, more than 500 million hectares have been treated with drones, resulting in significant water savings and reductions in carbon emissions.

Meeting Rising Food Demand and Sustainable Farming

With the global population approaching 10 billion, the pressure on agricultural productivity is higher than ever. Agriculture drones equipped with multispectral sensors help detect crop stress early, enabling precise nutrient or pesticide application without overuse. Studies, such as those conducted by the University of Florida, show drone-guided nutrient management can improve nitrogen efficiency by over 25% in certain crops. Consumers increasingly demand traceable, low-impact produce, while policies supporting sustainable farming further encourage the adoption of drone-based solutions.

Addressing Labor Shortages Through Automation

Labor scarcity is another factor boosting the agriculture drones market. Modern drones can be operated in swarms by a single pilot, allowing hundreds of acres to be covered efficiently. Rotor Technologies’ Sprayhawk, for example, can spray 240 acres per hour, rivaling light aircraft while reducing the need for manual labor. These solutions make aerial spraying accessible to mid-sized farms that previously lacked options for such services.

Carbon-Smart Farming and Incentives

Governments are increasingly offering subsidies and incentives for environmentally friendly practices. Drones provide low-cost, verifiable ways to monitor greenhouse gas emissions and field-level carbon metrics. Innovations like the University of São Paulo’s gas-sensing drone demonstrate how data collected from drones can be used to qualify for carbon credits, converting operational costs into potential revenue streams.

Market Segmentation: Agriculture Drones

The agriculture drones market is segmented by drone size, product type, service model, and application.

By Drone Size:

-

Small Drones (<20 kg): Accounted for 68% of unit shipments in 2024. Ideal for smaller farms, orchards, and irregular plots. Tank capacity typically ranges from 2.5–18 gallons, covering up to 50 acres per hour.

-

Medium Drones (20–150 kg): Projected to grow at a CAGR of 31% through 2030. Offer longer flight times, larger tanks, and enhanced automation for multi-drone operations. Medium drones are quickly becoming the backbone of large-scale precision agriculture.

By Service Model:

-

Product Sales: Represented 72% of market revenue in 2024, preferred by farms wanting full control over scheduling, maintenance, and data.

-

Drone-as-a-Service (DaaS): Expanding at 35% CAGR, DaaS allows smaller farms or those without trained pilots to access drone capabilities on-demand. Companies such as Hylio now offer multi-drone swarms for subscription services.

By Application:

-

Field Mapping: Accounts for 34% of revenue, providing baseline data for precision applications and crop analysis.

-

Variable-Rate Applications: Growing at 26.5% CAGR, this segment optimizes chemical use and supports seeding, cover crops, and beneficial insect distribution.

By Product Type:

-

Hardware: Comprising 64% of revenue in 2024, includes airframes, sensors, and propulsion systems.

-

Software: The fastest-growing segment with a 29% CAGR, software transforms raw drone imagery into actionable insights for crop management and input optimization.

Key Players in the Agriculture Drones Market

The agriculture drones market is moderately concentrated, with the top five players holding around 66% of global revenue.

-

DJI: Holds the largest share at 34%, leveraging scale and broad adoption.

-

XAG Co., Ltd.: Focused on Asia-Pacific markets with advanced medium-weight platforms.

-

Parrot SA: Offers industrial drones with specific agricultural applications.

-

AeroVironment Inc.: Specializes in precise, automated field solutions.

-

Trimble Inc.: Integrates drones with farm management systems for optimized decision-making.

Other notable developments include strategic partnerships, acquisitions, and innovations integrating artificial intelligence, swarm management, and carbon measurement tools to increase efficiency and monetization potential.

Conclusion: Outlook for the Agriculture Drones Market

The agriculture drones market is on track for strong growth between 2025 and 2030, driven by precision agriculture, labor constraints, sustainable farming policies, and expanding DaaS adoption. North America leads the market with 36% of revenue, while Asia-Pacific is the fastest-growing region at a 23% CAGR, thanks to initiatives in China, India, Japan, and South Korea. Medium-sized drones are gaining prominence, bridging the gap between small, affordable units and large, high-capacity systems.

Advancements in software, automation, and analytics are transforming drones from simple tools into integral farm management systems. As more farms adopt drones for mapping, spraying, and monitoring, the market is expected to deliver increased efficiency, cost savings, and sustainable crop production. The combination of technology adoption, regulatory support, and environmental incentives ensures a robust trajectory for the agriculture drones market over the coming years.

About Mordor Intelligence:

Mordor Intelligence is a trusted partner for businesses seeking comprehensive and actionable market intelligence. Our global reach, expert team, and tailored solutions empower organizations and individuals to make informed decisions, navigate complex markets, and achieve their strategic goals.

With a team of over 550 domain experts and on-ground specialists spanning 150+ countries, Mordor Intelligence possesses a unique understanding of the global business landscape. This expertise translates into comprehensive syndicated and custom research reports covering a wide spectrum of industries, including aerospace & defense, agriculture, animal nutrition and wellness, automation, automotive, chemicals & materials, consumer goods & services, electronics, energy & power, financial services, food & beverages, healthcare, hospitality & tourism, information & communications technology, investment opportunities, and logistics.