Introduction: Pet Care Market Overview

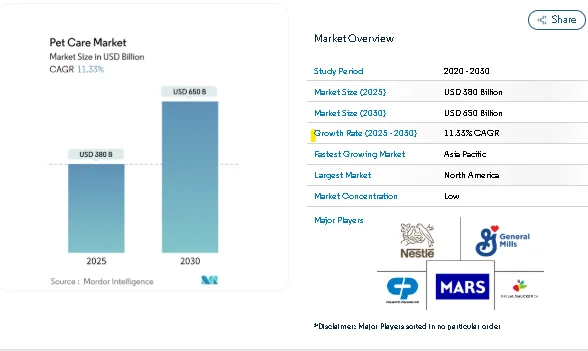

The global pet care market, valued at USD 380 billion in 2025, is projected to grow to USD 650 billion by 2030, reflecting a steady 11.33% CAGR. Increasing pet adoption, particularly among Millennials and Gen Z, is driving higher spending on pet food, healthcare, grooming, and wellness products. As pets increasingly become a part of households, owners are prioritizing premium nutrition, preventive health solutions, and technology-enabled services to improve the quality of life for their companions.

This market growth is further supported by urbanization in Asia-Pacific, growing disposable incomes, and the rising popularity of online retail and subscription-based platforms. Pet owners are investing more in functional and personalized diets, preventive healthcare, and innovative products, reinforcing premium pricing and brand loyalty.

Key Trends in the Pet Care Market

Rising Pet Ownership Among Millennials and Gen Z

Younger generations are driving a notable shift in pet care spending. In the U.S., Gen Z households owning pets increased by 43.5% between 2023 and 2024, reaching 18.8 million households. Similar growth is observed in China, where the urban pet population surpassed 120 million in 2024. These pet owners consider animals as family members and adjust their household budgets accordingly, prioritizing health, nutrition, and grooming over other discretionary expenses.

Humanization of Pets and Premium Spending

The humanization of pets is influencing product innovation and spending patterns. Premium dog food in the U.S. now represents 30% of category sales, with some owners spending up to USD 150 per month on high-quality, human-grade formulations. Fresh food options continue to grow rapidly, and preventive healthcare products like supplements and pet insurance are gaining traction, reflecting a strong willingness to invest in pets’ long-term wellness.

Expansion of E-Commerce and Subscription Models

Online retail and subscription platforms are reshaping the pet care landscape. U.S. e-commerce pet food sales are projected to exceed USD 21 billion in 2024, capturing 40% of the market. Platforms like Chewy are driving subscription adoption, enabling automated replenishment and personalized recommendations. Globally, online pet supplies are expected to grow from 6.4% penetration in 2023 to 8% by 2028, making digital channels an essential part of distribution strategies.

Advances in Nutrition Science

Functional and personalized diets are becoming mainstream. Brands such as Hill’s Pet Nutrition are leveraging microbiome-focused formulations to support digestive health, while alternative proteins like mealworm-based ingredients are gaining regulatory approval for pet food. These innovations provide sustainable, nutrient-rich options that meet pet owners’ expectations for health and environmental responsibility.

Inflation and Regulatory Challenges

Rising costs for ingredients and compliance pressures are influencing pricing strategies. Fifty-eight percent of owners believe pet products have become more expensive than other categories, and the median monthly dog ownership cost increased to USD 260 in 2024. Regulatory frameworks, including FDA and AAFCO guidelines, have tightened safety requirements, necessitating increased investment in testing, labeling, and product documentation.

Pet Care Market Segmentation

The pet care market is segmented by pet type, product type, distribution channel, price tier, and geography.

By Pet Type

-

Dogs: Dominant segment with 59% market share in 2024. Premium dog food and health products continue to drive revenue.

-

Cats: Experiencing a CAGR of 7.8% due to urban living trends and targeted cat products. Growth in single-person households contributes to increased adoption.

-

Others (Fish, Birds, Small Animals): Niche markets with stable demand for specialized nutrition and care products.

By Product Type

-

Pet Food: 40.5% of total market; fresh and refrigerated options growing at a 19.5% CAGR.

-

Healthcare Products: Supplements, medications, and preventive care items are expanding rapidly.

-

Grooming and Hygiene: High adoption for premium shampoos, conditioners, and hygiene tools.

-

Accessories and Services: Training, boarding, smart feeders, and connected devices enhance convenience and engagement.

By Price Tier

-

Mass: 63% of revenue in 2024, offering affordable and widely accessible products.

-

Premium and Super-Premium: Super-premium tier expected to grow at 15.2% CAGR, driven by life-stage nutrition, functional claims, and allergy-specific products.

By Distribution Channel

-

Offline Retail Stores: Accounted for 60% of sales in 2024; continue to benefit from in-person guidance.

-

Online Platforms & Subscription Services: Expected 18% CAGR growth; personalization and auto-replenishment drive loyalty.

-

Veterinary Channels: Offer credibility for diagnosis-linked products and professional-grade care items.

Key Players in the Pet Care Market

The competitive landscape is fragmented, with the five largest players holding just 14.7% of the total market. Leading companies include:

-

Mars Inc.: Expanded capabilities through acquisitions and digital investments in connected-care platforms.

-

Nestlé Purina: Focused on microbiome-based nutrition and sustainable protein options.

-

Colgate-Palmolive (Hill’s Pet Nutrition): Strong in functional and preventive healthcare products.

-

J.M. Smucker Co.: Offers specialty treats and premium pet products.

-

General Mills (Blue Buffalo): Growth via acquisition of Whitebridge Pet Brands to expand treat portfolios.

Smaller regional players and digitally native brands continue to capture niche markets, often focusing on raw diets, probiotics, and premium treats. Acquisition by larger firms remains common as these brands scale.

Conclusion: Future Outlook for the Pet Care Market

The global pet care market is set for significant growth through 2030, driven by rising pet ownership, premium nutrition, healthcare spending, and digital adoption. Dogs and cats remain the core focus for market expansion, while specialized products for smaller animals contribute to diversification.

With e-commerce and subscription models reshaping distribution, pet owners increasingly prefer convenience and personalized experiences. Despite inflation and regulatory challenges, the market maintains momentum as pet humanization encourages ongoing investment in quality nutrition, preventive health, and innovative products.

As households continue to integrate pets as family members, the pet care market will remain a dynamic and lucrative segment, offering opportunities for both established companies and emerging niche brands.

About Mordor Intelligence:

Mordor Intelligence is a trusted partner for businesses seeking comprehensive and actionable market intelligence. Our global reach, expert team, and tailored solutions empower organizations and individuals to make informed decisions, navigate complex markets, and achieve their strategic goals.

With a team of over 550 domain experts and on-ground specialists spanning 150+ countries, Mordor Intelligence possesses a unique understanding of the global business landscape. This expertise translates into comprehensive syndicated and custom research reports covering a wide spectrum of industries, including aerospace & defense, agriculture, animal nutrition and wellness, automation, automotive, chemicals & materials, consumer goods & services, electronics, energy & power, financial services, food & beverages, healthcare, hospitality & tourism, information & communications technology, investment opportunities, and logistics.