Introduction – Africa Ice Cream Market Overview

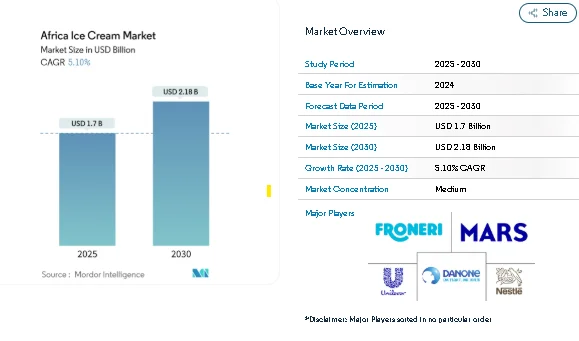

The Africa ice cream market is valued at USD 1.70 billion in 2025 and is projected to reach USD 2.18 billion by 2030, supported by steady development in distribution networks, expanding urban consumption, and increasing penetration into off-grid regions. Growth continues despite challenges such as dairy supply instability, sugar taxes, and pressure on ingredient costs. While multinational companies have scaled back capital-heavy manufacturing models, regional and local players are actively widening access through flexible production, mobile vendors, and solar-powered micro-distribution systems. These shifts reflect a market that is expanding its geographic reach rather than relying solely on per-capita intake increases.

The Africa ice cream market is influenced by evolving consumer behavior, the rise of experiential retail formats, and increasing demand for natural flavors. These dynamics are further reinforced by the broader food and beverages market trends across the continent, contributing to the beverages market analysis included in many regional strategy reviews.

Key Trends – Africa Ice Cream Market Trends

The Africa ice cream market is shaped by several interconnected trends that influence pricing, formulation, retail expansion, and distribution strategies.

Rising Urban Incomes and Changing Consumption Behaviour

Growing incomes in cities such as Nairobi, Lagos, and Accra continue to influence category segmentation, with premium products gaining visibility in modern retail. However, inflation-driven volatility still controls purchasing power, further boosting the need for smaller pack sizes and value formats. Youth populations increasingly turn to convenient frozen treats as occasional indulgence foods, intensifying demand for impulse formats, take-home tubs, and affordable street-vendor offerings.

Expansion of Modern Retail Infrastructure

Supermarkets and hypermarkets are gradually improving cold-chain consistency, enabling structured frozen aisles and better merchandising. Retail chains are adding dedicated freezer space that strengthens brand visibility. At the same time, informal kiosks, independent convenience stores, and mobile vendors remain essential for volume, requiring producers to maintain dual-channel strategies. Portable solar freezers, now used in several East African markets, allow brands to reach areas that previously lacked reliable electricity.

Demand for Natural and Localized Flavors

Consumers are increasingly aware of ingredient labels, driving interest in natural flavors, fruit-based options, and local ingredients like baobab. Artisanal brands across South Africa and Kenya are tapping into this preference through small-batch production and indigenous flavors. This trend is particularly strong in affluent urban clusters where shoppers are willing to explore new taste profiles.

Cold-Chain Limitations in Rural Areas

Rural regions still face limited cold-chain reach, affecting on-shelf availability and constraining market penetration. While solar-powered infrastructure is scaling gradually, it requires coordinated investment and distributor networks to be sustainable. These gaps present both challenges and opportunities, especially for producers targeting low-income and remote communities.

Volatile Dairy Prices and Formulation Adjustments

Price fluctuations in fresh milk supply are driving producers to adjust formulations using alternatives such as milk powder or plant-based fats. While these choices help stabilize cost structures, they require careful balancing to meet regulatory guidelines and maintain consumer trust.

Market Segmentation – Africa Ice Cream Market Segments

The Africa ice cream market spans a diverse mix of products, flavors, formats, and channels. Each segment reflects specific demand drivers and consumption behaviors.

By Product Type

-

Impulse Ice Cream – Popular among youth and mobile consumers seeking immediate, low-cost indulgence.

-

Take-Home Ice Cream – Favoured in urban households with access to home refrigeration.

-

Artisanal Ice Cream – Expanding among premium shoppers in major cities through parlors and boutique retail.

By Flavor

-

Chocolate – Maintains dominance due to familiarity and broad consumer appeal.

-

Fruit – Benefiting from interest in natural ingredients and tropical fruit-based formulations.

-

Others – Includes vanilla, nut-based varieties, and local specialties used by artisanal brands.

By Form

-

Cups and Tubs – Serve home-based consumption and family gatherings.

-

Bars and Sticks – Drive impulse buying through kiosks and street vendors.

-

Cones – Often consumed on-premise at parlors and dine-in outlets.

By Distribution Channel

-

On-Trade – Includes cafes, restaurants, quick-service outlets, and ice cream parlors.

-

Off-Trade – Involves supermarkets, hypermarkets, convenience stores, specialist stores, and online channels.

By Geography

-

South Africa – Strongest retail infrastructure and highest per-capita consumption.

-

Nigeria – Large population, expanding youth demand, growing urban retail formats.

-

Kenya, Tanzania, Ghana – Building cold-chain capabilities and increasing flavor innovation.

-

Rest of Africa – Early-stage markets with long-term potential through solar-powered distribution models.

Key Players – Africa Ice Cream Market Competitive Landscape

The Africa ice cream market includes multinational corporations, regional manufacturers, and artisanal brands that cater to diverse consumer groups. Global companies such as Nestlé, Unilever, Danone, Froneri, and Mars operate across major markets through flexible production structures, often relying on contract manufacturing and franchised distribution to reduce operational risk. Their brand portfolios benefit from established global flavor lines, marketing capabilities, and research resources.

Regional producers contribute significantly in East, West, and Southern Africa by leveraging local sourcing, cost-efficient operations, and deep familiarity with consumer preferences. These firms serve both modern retail and informal trade, including mobile vendors and community kiosks.

Artisanal businesses are expanding their presence in major urban centers by offering clean-label products, indigenous flavors, and chef-driven experiences. Their premium pricing reflects small-batch production and localized ingredient use, appealing to niche but steadily growing consumer groups. Across these layers, the competitive environment remains active and dynamic, documented widely in beverages market industry analysis and beverages market industry report references due to overlapping retail and cold-chain infrastructure.

Conclusion – Outlook for the Africa Ice Cream Market

The Africa ice cream market is on a stable growth trajectory supported by increasing urbanization, youth-driven demand, and continued improvements in distribution. While cold-chain limitations, dairy supply volatility, and regulatory compliance remain challenges, producers are adopting more flexible business models to maintain market reach. The rise of artisanal offerings, growing presence in supermarkets, expanding mobile vending, and improved energy-efficient cold-chain systems are creating new opportunities.

As the beverages market size continues to shape consumer retail patterns, ice cream is increasingly integrated into broader food and beverage strategies across the region. With innovation in formats, flavors, and distribution, the market is expected to evolve steadily through 2030, appealing to both entry-level buyers and premium seekers across Africa.

About Mordor Intelligence:

Mordor Intelligence is a trusted partner for businesses seeking comprehensive and actionable market intelligence. Our global reach, expert team, and tailored solutions empower organizations and individuals to make informed decisions, navigate complex markets, and achieve their strategic goals.

With a team of over 550 domain experts and on-ground specialists spanning 150+ countries, Mordor Intelligence possesses a unique understanding of the global business landscape. This expertise translates into comprehensive syndicated and custom research reports covering a wide spectrum of industries, including aerospace & defense, agriculture, animal nutrition and wellness, automation, automotive, chemicals & materials, consumer goods & services, electronics, energy & power, financial services, food & beverages, healthcare, hospitality & tourism, information & communications technology, investment opportunities, and logistics.