Introduction: Saudi Arabia Poultry Sector Market Overview

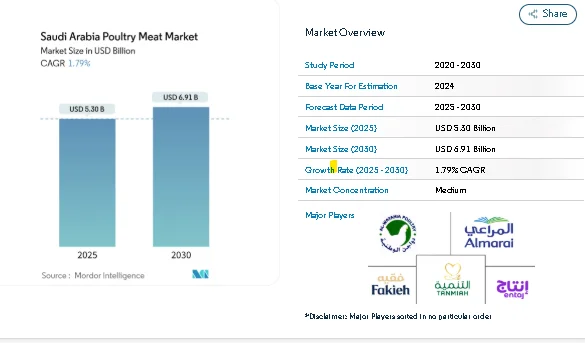

The Saudi Arabia poultry sector continues to strengthen its footprint as one of the most strategically supported food industries in the Kingdom. With a market value of USD 5.30 billion in 2025, the sector is projected to reach USD 6.91 billion by 2030, marking steady progress as the country works toward its Vision 2030 food-security goals. Rising domestic production, large-scale private investments, and expanded government financing have helped the poultry industry reduce import reliance and build a more resilient supply chain.

Growing population numbers, higher per-capita poultry consumption, and increasing demand for fresh, halal-certified products are shaping the sector’s long-term direction. At the same time, shifts in consumer behavior—especially toward convenience, value-added products, and online purchasing—continue to change how poultry products are produced, processed, and distributed across the Kingdom.

Key Trends Shaping the Saudi Arabia Poultry Sector

1. Vision 2030 Investment Support Strengthens Production Capacity

The Saudi government’s continuous focus on food security remains a major growth driver for the poultry sector. Vision 2030 allocates substantial funding to expanding local poultry production and aims to lift self-sufficiency levels toward 90% by 2030.

Through the Agricultural Development Fund, up to 70% financing is provided for qualified poultry projects. Many companies are using this support to scale their hatcheries, breeding farms, and processing operations. New integrated farms, advanced processing lines, and improved cold-chain infrastructure have enhanced production efficiency while encouraging private-sector partnerships.

Regulatory improvements through the Saudi Food and Drug Authority (SFDA)—such as streamlined licensing, digital inspections, and unified halal standards—have added further momentum, reducing delays and improving operational predictability for producers.

2. High Poultry Consumption Fueled by Demographic and Lifestyle Shifts

Poultry remains the preferred protein source for Saudi households, and rising consumption patterns continue to expand market demand. A growing youth population, fast-paced urban lifestyles, and increasing interest in health-focused diets have all contributed to higher intake of poultry products.

Demand is shifting toward:

-

Fresh and chilled poultry for daily cooking

-

Value-added and marinated products for convenience

-

Organic and free-range poultry as part of healthier meal choices

Private-label brands are gaining traction as well, with a strong share of Saudi consumers now purchasing store-brand poultry products across modern retail channels.

3. Expansion of Modern Retail and Digital Sales Channels

Supermarkets, hypermarkets, and convenience stores continue to anchor poultry distribution, while online retail is quickly becoming a strong secondary channel. Retail chains such as Spinneys and Circle K are expanding their footprints, attracting consumers seeking quality assurance and variety through modern retail displays.

E-commerce platforms and online food delivery services have introduced new ways for consumers to purchase fresh and processed poultry. Digital channels benefit from detailed product listings, traceability information, and efficient last-mile cold-chain logistics—helping manufacturers reach a wider customer base and underserved regions.

4. Growing Demand for Halal-Certified Local Poultry

SFDA’s updated halal certification rules have elevated product quality and strengthened trust in domestic producers. All imported and processed poultry now requires certification from approved bodies, making compliance a central aspect of market participation.

These standards support:

-

Stronger consumer preference for fresh local poultry

-

Improved traceability across the supply chain

-

Opportunities for Saudi producers to export to halal-focused markets

This shift creates a more competitive environment for domestic companies, while international suppliers must now adapt to stricter guidelines to maintain access.

Market Segmentation: Saudi Arabia Poultry Sector

By Form

The Saudi poultry sector is segmented into Canned, Fresh/Chilled, Frozen, and Processed categories.

Fresh/Chilled Poultry – Leading Segment

-

Holds the highest share due to cultural preference for fresh meat

-

Supported by expanded cold-chain systems and modern retail growth

Processed Poultry – Fastest Growing Category

-

Driven by increasing urbanization and demand for convenience

-

Includes marinated items, nuggets, sausages, deli meats, and ready-to-cook choices

-

Strong opportunities in private-label manufacturing

Frozen and Canned Poultry maintain steady relevance but face slower growth compared to fresh and processed formats.

By Distribution Channel

The sector includes Off-Trade (supermarkets, online channels, convenience stores) and On-Trade (restaurants, hotels, catering) channels.

Key highlights:

-

Supermarkets & Hypermarkets remain the dominant distribution channel

-

Online Channels show the highest growth rate as consumers adapt to digital shopping

-

Restaurants and Catering continue to expand demand for processed and portioned poultry

Key Players in the Saudi Arabia Poultry Sector

The market features a mix of large domestic corporations and multinational companies. Leading players include:

-

Al-Watania Poultry

-

Almarai (Alyoum Poultry)

-

Tanmiah Food Company

-

Fakieh Poultry Farms

-

Entaj

These companies benefit from integrated operations that cover breeding, farming, feed production, processing, packaging, and broad distribution networks. International producers such as BRF and JBS also play a significant role by establishing local facilities to meet Saudi halal and production requirements.

Conclusion

The Saudi Arabia poultry sector is entering a period of stable and strategic growth supported by national food-security initiatives, rising consumer demand, and expanded retail ecosystems. As production capacity increases and technology-driven farming becomes more common, the Kingdom is expected to further strengthen its position as a leading poultry market in the Gulf region.

Rising interest in fresh, halal-certified, and convenience-driven poultry products will continue to push innovation in processing and distribution. With steady government backing, growing digital adoption, and higher private-sector participation, the poultry industry is well positioned to reach its forecasted USD 6.91 billion valuation by 2030, reinforcing its importance within Saudi Arabia’s long-term economic landscape.

About Mordor Intelligence:

Mordor Intelligence is a trusted partner for businesses seeking comprehensive and actionable market intelligence. Our global reach, expert team, and tailored solutions empower organizations and individuals to make informed decisions, navigate complex markets, and achieve their strategic goals.

With a team of over 550 domain experts and on-ground specialists spanning 150+ countries, Mordor Intelligence possesses a unique understanding of the global business landscape. This expertise translates into comprehensive syndicated and custom research reports covering a wide spectrum of industries, including aerospace & defense, agriculture, animal nutrition and wellness, automation, automotive, chemicals & materials, consumer goods & services, electronics, energy & power, financial services, food & beverages, healthcare, hospitality & tourism, information & communications technology, investment opportunities, and logistics.