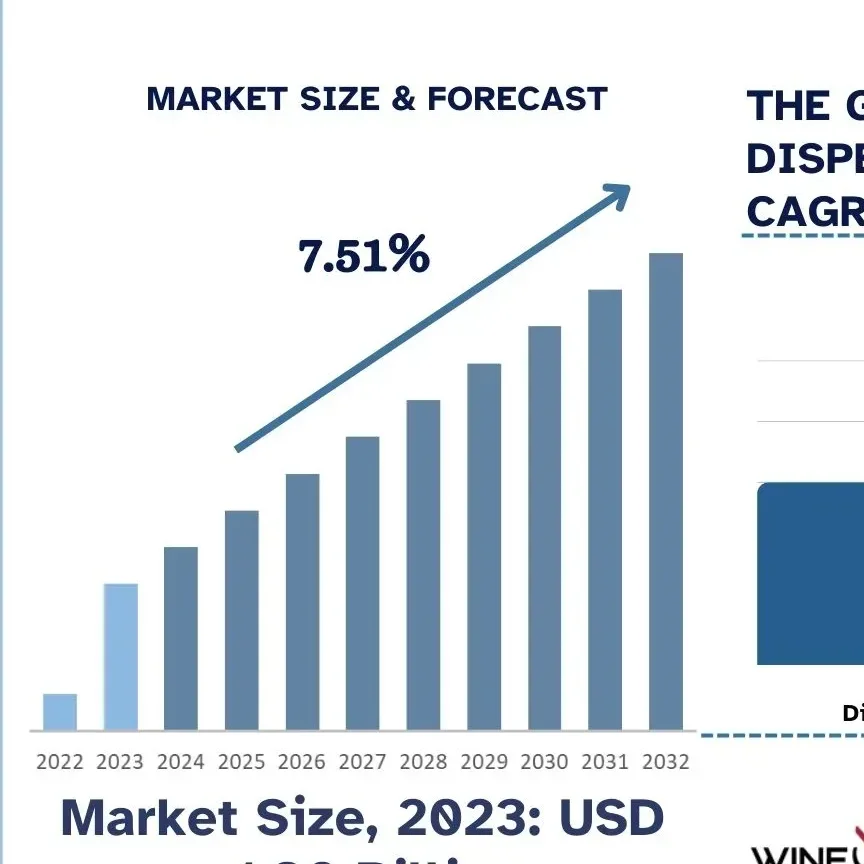

The global satellite communication market size was valued at USD 90.30 billion in 2024 and is expected to reach USD 159.60 billion by 2030, expanding at a CAGR of 10.2% from 2025 to 2030. Market growth is primarily driven by the rising adoption of High-Throughput Satellite (HTS) systems, which deliver substantially higher data speed and capacity compared to traditional satellite solutions. Their ability to support bandwidth-heavy applications such as video streaming, IoT connectivity, and remote sensing continues to accelerate demand across industries.

Key Market Trends & Insights

- The Asia Pacific satellite communication market captured 23.7% of global share in 2024.

- The U.S. maintained a dominant position in 2024.

- By component, the services segment accounted for the largest share at 58.8% in 2024.

- By frequency band, the Ku-band remained the leading segment in 2024.

- By application, broadcasting dominated the market.

- By vertical, media & broadcasting remained the primary revenue contributor.

Market Size & Forecast

- 2024 Market Size: USD 90.30 Billion

- 2030 Market Size Forecast: USD 159.60 Billion

- CAGR (2025–2030): 10.2%

- Asia Pacific: Largest regional market in 2024

HTS systems have become essential for next-generation communication infrastructure due to their ability to facilitate rapid and reliable data transfer. These capabilities make them highly suitable for emerging use cases that demand high bandwidth efficiency. In parallel, the introduction of advanced high-frequency and very high-frequency bands is further widening the satcom spectrum, enabling higher capacity and enhanced data rates.

Global satellite solution providers are actively developing innovative products to meet diverse industry needs. For instance, in June 2023, Get SAT Ltd launched its MoComm product line featuring multi-orbit communication, enabling seamless switching between different satellite constellations. MoComm supports both Ku-band and Ka-band, allowing smooth data movement between GEO, MEO, and LEO networks while expanding overall operational flexibility.

Demand from the government and defense sectors is also rising significantly, driven by increased reliance on ISR platforms, high-definition video transmission, and continuous connectivity for UAV and RPAS systems. Major players such as Viasat, Inc. and SES S.A. continue to invest in advanced satcom technologies to support mission-critical operations across these sectors.

Order a free sample PDF of the Satellite Communication Market Intelligence Study, published by Grand View Research.

Key Satellite Communication Company Insights

The satellite communication market is characterized by strong competition, with leading companies expanding their global reach through partnerships, mergers, acquisitions, and advanced technology offerings.

- Viasat, Inc. offers end-to-end communication platforms, including ground infrastructure, Ka-band satellites, and high-speed broadband solutions.

- Intelsat S.A. delivers data, voice, and video transmission services to telecom operators, ISPs, media companies, and global enterprises.

Leading Satellite Communication Companies

- Viasat, Inc.

- SES S.A

- Intelsat S.A.

- Telesat Corporation

- EchoStar Corporation

- L3Harris Technologies, Inc.

- Thuraya Telecommunications Company (Yashat)

- SKY Perfect JSAT Holdings Inc.

- Gilat Satellite Networks Ltd.

- Cobham Limited

Conclusion

The satellite communication market is advancing rapidly due to increasing demand for high-capacity networks, expansion of multi-orbit solutions, and rising adoption across government, defense, and commercial sectors. HTS technology, spectrum expansion, and strategic investments by industry leaders are set to further strengthen market growth. With robust opportunities emerging across global regions, the market is poised for sustained expansion through 2030.

Explore Horizon Databook – The world’s most expansive market intelligence platform developed by Grand View Research.