Section 44AD of the Income Tax Act, 1961 introduces the concept of presumptive taxation for eligible taxpayers. The objective of this provision is to simplify tax compliance for small businesses by reducing the burden of maintaining detailed books of accounts and undergoing tax audits. Section 44AD presumptive taxation is especially relevant for resident individuals, Hindu Undivided Families (HUFs), and partnership firms engaged in small-scale business activities.

This article by Mohit S. Shah & Co explains the meaning, scope, eligibility, calculation method, advantages, limitations, and compliance requirements related to Presumptive Taxation for Small Businesses in India, with specific reference to Section 44AD and ITR filing for small businesses in India.

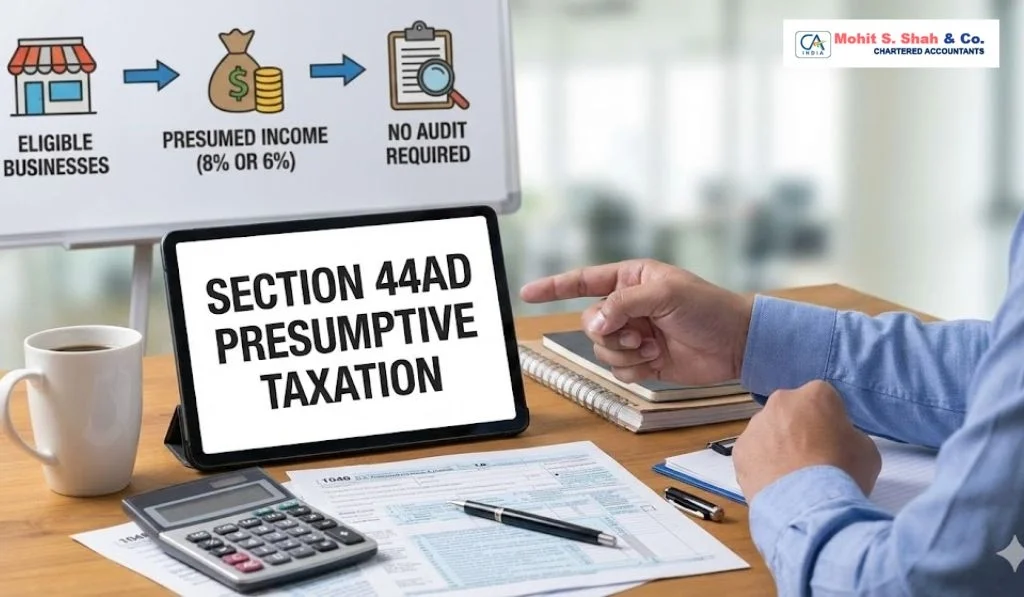

Meaning of Section 44AD Presumptive Taxation

Section 44AD presumptive taxation allows eligible taxpayers to declare income at a prescribed percentage of their total turnover or gross receipts instead of calculating actual profits. The law presumes that a fixed percentage of turnover represents taxable income, thereby eliminating the need for detailed expense tracking.

Under Section 44AD:

-

Income is presumed at 8% of total turnover, or

-

6% of turnover received through digital modes (such as bank transfer, UPI, or cheque)

This approach helps small businesses comply with tax requirements in a simplified manner.

Presumptive Taxation for Small Businesses in India

Presumptive Taxation for Small Businesses in India was introduced to reduce compliance costs and encourage voluntary tax reporting. Small businesses often find it difficult to maintain detailed accounting records or afford professional audits. Section 44AD addresses this concern by offering a simplified taxation scheme.

The scheme is optional. Eligible taxpayers may choose between:

-

Normal provisions of taxation, or

-

Presumptive taxation under Section 44AD

Once chosen, certain conditions apply, which are explained later in this article.

Eligibility Criteria under Section 44AD

To avail benefits under Section 44AD, the following conditions must be satisfied:

Eligible Taxpayers

-

Resident individuals

-

Resident Hindu Undivided Families (HUFs)

-

Resident partnership firms (excluding LLPs)

Eligible Businesses

-

Any business except:

-

Profession referred under Section 44AA(1)

-

Agency business

-

Business earning commission or brokerage income

-

Turnover Limit

-

Total turnover or gross receipts should not exceed ₹2 crore during the financial year

If these conditions are met, the taxpayer may opt for Section 44AD presumptive taxation.

Income Calculation under Section 44AD

Income under Section 44AD is calculated as follows:

-

8% of turnover for cash receipts

-

6% of turnover for digital receipts

The taxpayer may declare higher income than the prescribed percentage if actual profits are higher. However, declaring lower income than the presumptive rate is allowed only if:

-

Books of accounts are maintained, and

-

Tax audit under Section 44AB is conducted (if applicable)

This structure makes Section 44AD suitable for businesses with stable margins.

Treatment of Expenses and Deductions

Under Section 44AD:

-

All business expenses are presumed to be allowed

-

No separate deduction is permitted for rent, salary, depreciation, or interest

However, depreciation is deemed to have been allowed, and the written down value of assets must be adjusted accordingly.

For partners in a partnership firm, remuneration and interest to partners are considered included in the presumptive income and cannot be claimed separately.

Applicability of Advance Tax under Section 44AD

Taxpayers opting for Section 44AD are required to pay 100% of advance tax by 15th March of the financial year. Quarterly advance tax installments are not required under this scheme.

Failure to pay advance tax on time may attract interest under Sections 234B and 234C.

Continuity Requirement and Five-Year Rule

Once a taxpayer opts for Section 44AD presumptive taxation, continuity is required for five consecutive assessment years.

If the taxpayer:

-

Opts out before completing five years, and

-

Declares income under normal provisions

Then:

-

The taxpayer becomes ineligible for Section 44AD for the next five years

This rule is important to consider before choosing the presumptive scheme.

ITR Filing for Small Businesses in India under Section 44AD

ITR filing for small businesses in India opting for Section 44AD is comparatively simple.

Applicable ITR Form

-

ITR-4 (Sugam) is used for taxpayers opting for presumptive taxation under Section 44AD

Key Features of ITR-4

-

No requirement to upload balance sheet or profit & loss account

-

Limited disclosure of financial details

-

Faster filing and processing

However, taxpayers must ensure that:

-

All income sources are correctly reported

-

Presumptive income is accurately calculated

-

Other incomes such as interest or capital gains are disclosed separately

Advantages of Section 44AD Presumptive Taxation

Section 44AD offers several practical benefits:

-

Reduced compliance burden

-

No mandatory maintenance of detailed books

-

No tax audit requirement (subject to conditions)

-

Simplified income calculation

-

Time and cost efficiency for small taxpayers

These features make Presumptive Taxation for Small Businesses in India a widely used option.

Limitations and Points of Caution

Despite its benefits, Section 44AD has certain limitations:

-

Not suitable for businesses with low profit margins

-

Five-year lock-in requirement restricts flexibility

-

Not applicable to professionals or LLPs

-

Deductions under Chapter VI-A are allowed, but business expenses are not separately claimable

Taxpayers should evaluate business profitability before opting for the scheme.

Common Misconceptions about Section 44AD

Some common misunderstandings include:

-

Section 44AD is mandatory (it is optional)

-

Taxpayers cannot declare higher income (they can)

-

GST compliance is not required (GST laws are separate)

Clear understanding helps avoid compliance errors during ITR filing for small businesses in India.

Conclusion

Section 44AD presumptive taxation is a simplified tax mechanism designed to ease compliance for eligible small businesses. By allowing income declaration at a fixed percentage of turnover, it reduces the need for extensive accounting and audits. However, the scheme comes with specific conditions, eligibility criteria, and long-term implications.

This overview by Mohit S. Shah & Co aims to provide a clear and factual understanding of Section 44AD, Presumptive Taxation for Small Businesses in India, and related aspects of ITR filing for small businesses in India, helping taxpayers make informed compliance decisions in line with Indian income tax laws.