Introduction to the Refractories Market Landscape

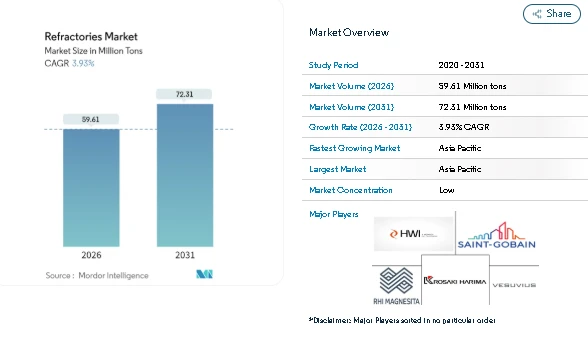

The Refractories Market plays a vital role in supporting industries that operate under extreme heat and chemical stress. According to the Mordor Intelligence assessment, the Refractories Market Size stood at 57.36 million tons in 2025, increased to 59.61 million tons in 2026, and is projected to reach 72.31 million tons by 2031, reflecting steady Refractories Market Growth over the forecast period.

The Refractories Market Forecast suggests that demand will remain resilient as producers focus on longer service life, compliance with environmental standards, and consistent thermal performance.

Industry Dynamics of the Refractories Market

Steel Production Shifts and Process Optimization

Iron and steel manufacturing remains the backbone of the Refractories Market. Steel producers are increasingly focusing on process efficiency, furnace life extension, and energy optimization. As steel plants modernize equipment and retire older units, refractory selection is becoming more application-specific, supporting value-based demand within the Refractories Industry.

Environmental Compliance and Material Choices

Environmental regulations are influencing refractory formulation and usage patterns. Producers are giving preference to materials that reduce dust exposure, lower emissions during installation, and support recycling initiatives. These requirements are shaping Refractories Market Trends, particularly in regions with strict occupational and environmental standards.

Energy, Chemicals, and Alternative Fuel Use

Energy and chemical industries are steadily contributing to Refractories Market Growth. The increasing use of alternative fuels and complex feedstocks in kilns and reactors exposes linings to aggressive conditions. This has increased the focus on refractories with improved resistance to chemical attack and thermal cycling.

Expansion of High-Temperature Ceramic Applications

Beyond traditional sectors, high-temperature ceramic applications such as battery material processing and waste-to-energy systems are creating new avenues within the Refractories Market. These applications demand precise thermal control and material purity, encouraging suppliers to diversify offerings while staying within core refractory expertise.

Refractories Segment Analysis Overview

-

Non-clay Refractories

-

Magnesite Brick

-

Zirconia Brick

-

Silica Brick

-

Chromite Brick

-

Other (Carbides, Silicates)

-

Clay Refractories

-

High-Alumina

-

Fireclay

-

Insulating

By End-User Industry:

-

Iron and Steel

-

Cement

-

Energy and Chemicals

-

Non-Ferrous Metals

-

Glass

-

Ceramic

-

Other End-user Industries (Pulp and Paper, Waste-to-Energy)

By Geography:

-

Asia-Pacific

-

China

-

India

-

Japan

-

South Korea

-

Rest of Asia-Pacific

-

North America

-

United States

-

Canada

-

Mexico

-

Europe

-

Germany

-

United Kingdom

-

France

-

Italy

-

Russia

-

Rest of Europe

-

South America

-

Brazil

-

Argentina

-

Rest of South America

-

Middle East and Africa

-

Saudi Arabia

-

South Africa

-

Rest of Middle East and Africa

Refractories Industry Competitive Landscape Overview

-

Krosaki Harima Corporation

-

RHI Magnesita

-

Vesuvius

-

Saint-Gobain

-

HarbisonWalker International

Conclusion

The Refractories Market remains a key part of global industry, driven by steady demand from steel, cement, energy, and chemical sectors. Growth is steady, supported by maintenance, capacity upgrades, and evolving production needs. Suppliers balancing performance, cost, and service are best positioned, making the market essential for high-temperature industrial operations worldwide.