Introduction to the Space Electronics Market

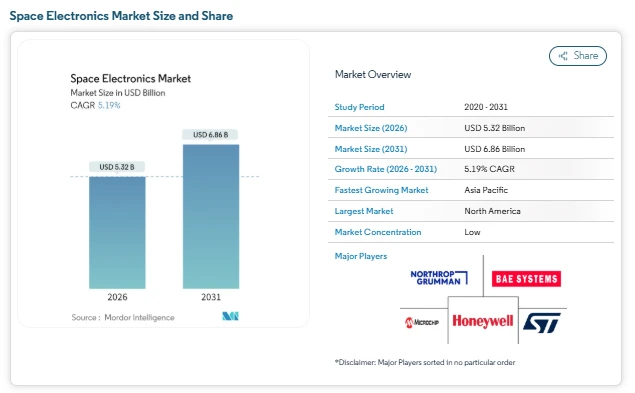

The global Space Electronics Market size is on a steady growth path, projected to rise from USD 5.32 billion in 2026 to USD 6.86 billion by 2031. This expansion reflects increasing demand for advanced onboard electronics across satellites, launch vehicles, and deep-space probes. As satellite constellations scale up, deep-space missions grow more complex, and small satellite production becomes more commercialized, the market is witnessing a shift from experimental prototypes toward high-volume, radiation-tolerant, and high-performance electronics.

The growth of this market is closely tied to the rising adoption of autonomous onboard systems, high-efficiency power devices, and integrated circuits capable of operating in extreme radiation and temperature conditions.

Key Trends in the Space Electronics Market

Rapid Deployment of Large LEO Satellite Constellations

A major driver for the Space Electronics Market Trends is the rapid deployment of large low Earth orbit (LEO) constellations. Modern small satellites are increasingly heavier and more capable, incorporating high-performance processors, memory, and optical communication systems while remaining within tight launch cost constraints.

Increasing Deep-Space Exploration Missions

Deep-space missions, such as lunar and Mars exploration, are shaping the Space Electronics Market Industry through demand for processors that can operate autonomously over long distances with extreme radiation tolerance. NASA’s High-Performance Spaceflight Computing initiative exemplifies the need for fault-tolerant, AI-accelerated processors capable of performing complex navigation and scientific tasks without real-time ground intervention.

On-Board Edge-AI and High-Bandwidth Payload Processing

The adoption of edge-AI in spacecraft is transforming the market by reducing data downlink requirements by up to 90%, enabling real-time decision-making in orbit. Advanced GPUs and neuromorphic processors are now being tested in flight, delivering high computational performance within space-rated thermal and radiation constraints

Miniaturization and Mass Production of Small Satellites

Small satellite platforms continue to drive demand for compact, multifunctional electronics. MEMS-based sensors, modular avionics, and system-on-chip designs allow for higher payload density while maintaining electromagnetic compatibility. Mass production practices, adapted from consumer electronics, now enable dozens of satellites to be assembled monthly.

Market Segmentation of the Space Electronics Market

By Platform

-

Satellites

-

Launch Vehicles

-

Deep Space Probes

-

Space Stations

By Application

-

Communication

-

Earth Observation

-

Navigation and Surveillance

-

Scientific and Technology Demonstration

-

Other Applications

By Component

-

Integrated Circuits

-

Power Devices

-

Sensors and MEMS

-

RF and Microwave Devices

-

Discrete Semiconductors and Opto-electronics

By Type

-

Radiation-Hardened

-

Radiation-Tolerant

By End-User

-

Commercial

-

Military and Defense

-

Civil Government and Space Agencies

Geography

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East and Africa

-

Middle East

-

Africa

Key Players in the Space Electronics Market

The Space Electronics Market Industry Leaders include established aerospace and semiconductor firms that supply both commercial and defense applications. Key companies include:

-

Microchip Technology Inc.

-

BAE Systems plc

-

Honeywell International Inc.

-

Northrop Grumman Corporation

-

STMicroelectronics NV

These firms leverage decades of experience in rad-hard electronics, flight processors, and power devices. Competitive differentiation in this market now emphasizes computational throughput per watt, radiation resilience per dollar, and rapid qualification cycles. Partnerships between traditional aerospace companies and commercial semiconductor developers have accelerated development of power-conversion ASICs and AI-capable processors, creating a dynamic competitive landscape.

Conclusion

The Space Electronics Market is poised for steady growth, driven by expanding satellite constellations, deep-space exploration, onboard AI, and small-satellite production. While challenges such as rad-hard wafer bottlenecks and regulatory compliance persist, collaborative strategies between space-heritage and commercial firms are enabling innovation to reach flight-ready applications faster.

Overall, the Space Electronics Market Size is expected to grow substantially by 2031, with evolving trends in edge-AI, wide-bandgap power technologies, and miniaturized satellite systems shaping the market’s future. These factors reinforce the importance of strategic investment and innovation within the Space Electronics Market Industry, positioning it as a critical segment of the global aerospace sector.