Europe Light Commercial Vehicles Market Overview

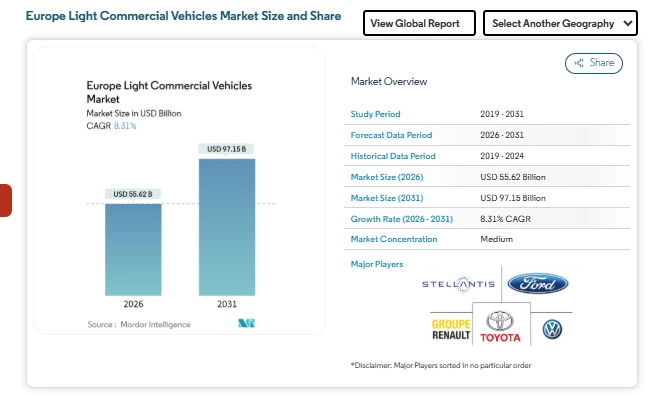

The Europe light commercial vehicles market size continues to play a central role in regional logistics, trade services, and urban mobility. According to Mordor Intelligence, the market was valued at USD 55.62 billion in 2026 and is projected to reach USD 97.15 billion by 2031, reflecting steady expansion during the forecast period. This outlook highlights how light commercial vehicles remain essential to delivery networks, utilities, construction, and public services across Europe.

The Europe light commercial vehicles industry is benefiting from the rise of e-commerce, stricter city emission rules, and changing fleet ownership models. Operators are adjusting vehicle choices to meet daily delivery needs while aligning with regulatory expectations in major cities. As a result, fleet renewal activity remains active across Western and Northern Europe, while adoption gradually spreads across Southern and Eastern markets.

Europe Light Commercial Vehicles Market Trends Shaping Demand

Shift Toward Electric and Low-Emission Vans

Urban fleets are increasingly choosing electric and low-emission vans to ensure unrestricted access to city centers and comply with local emission rules.

Rising Demand for Compact and Mid-Weight Vehicles

Delivery operators prefer smaller and mid-weight vehicles that can move easily through congested streets while still carrying practical payloads.

Increasing Preference for Leasing and Rental Models

Businesses are turning to leasing and rental options to reduce upfront costs and maintain flexibility as vehicle technologies and regulations continue to change.

Europe Light Commercial Vehicles Market Segmentation

By Vehicle Type

-

Light Commercial Vans

-

Light Pick-up Trucks (Less than 3.5 t GVW)

-

Chassis-Cab / Platform Cab

-

Mini-Trucks / Micro-LCVs

-

Minibuses (Less than 20 seats)

By Gross Vehicle Weight (GVW) Class

-

Less than 2.0 t

-

2.1 to 2.5 t

-

2.6 to 3.0 t

-

3.1 to 3.5 t

-

3.6 to 5.0 t

By Propulsion Type

-

BEV (Battery Electric Vehicle)

-

PHEV (Plug-in Hybrid Electric Vehicle)

-

HEV (Hybrid Electric Vehicle)

-

FCEV (Fuel Cell Electric Vehicle)

-

ICE (Internal Combustion Engine)

By End-Use Industry

-

Urban Last-Mile Delivery and Courier

-

Utilities and Field Services

-

Construction and Building Supplies

-

Postal and Parcel

-

Agriculture and Rural Services

-

Mobile Workshops and Special Purpose

By Ownership / Fleet Type

-

Corporate Fleets

-

SME Fleets

-

Self-Employed / Sole Proprietors

-

Rental and Leasing Companies

-

Government and Municipal Fleets

By Country

-

Austria

-

Belgium

-

Czech Republic

-

Denmark

-

Estonia

-

France

-

Germany

-

Ireland

-

Italy

-

Latvia

-

Lithuania

-

Norway

-

Poland

-

Russia

-

Spain

-

Sweden

-

United Kingdom

-

Rest of Europe

Competitive Landscape in the Europe Light Commercial Vehicles Industry

The Europe light commercial vehicles industry features a competitive mix of established automotive groups and newer entrants offering electric-focused lineups. Major manufacturers maintain strong positions through broad portfolios, established dealer networks, and long-standing fleet relationships.

Key players include:

-

Ford Motor Company

-

Volkswagen AG

-

Stellantis N.V.

-

Renault Group

-

Toyota Motor Corporation

Conclusion: Europe Light Commercial Vehicles Market

The Europe light commercial vehicles market forecast reflects a balanced mix of regulatory influence, commercial demand, and operational practicality. Growth is supported by delivery activity, public service requirements, and gradual fleet renewal across countries.

While adoption patterns vary by region and use case, the overall Europe light commercial vehicles market size is expected to expand as businesses adjust to urban access rules and evolving customer expectations. Manufacturers that offer reliable, adaptable, and cost-effective vehicles are well positioned within the Europe light commercial vehicles industry over the coming years.

As logistics, utilities, and service sectors continue to depend on light commercial vehicles, the market remains a key component of Europe’s transport and economic infrastructure.