Introduction

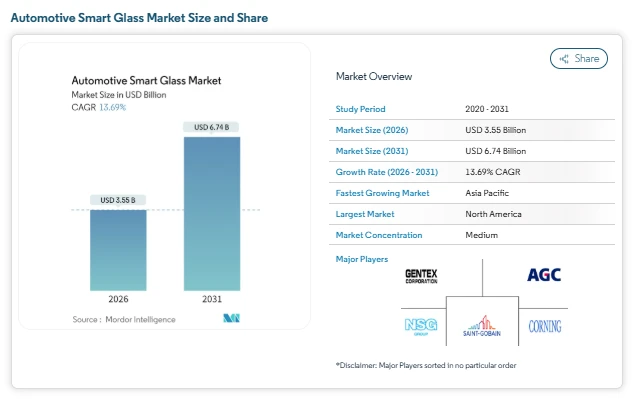

The automotive smart glass market is entering a decisive growth phase as automakers focus on cabin comfort, energy efficiency, and advanced vehicle design. According to Mordor Intelligence, the automotive smart glass market size is estimated at USD 3.55 billion in 2026, and projected to reach USD 6.74 billion by 2031, supported by a 13.69% CAGR during the forecast period.

This expansion reflects the growing use of switchable glazing across sunroofs, windshields, and side windows, particularly in electric and premium passenger vehicles. Smart glass enables real-time control of light and heat without mechanical shades, helping automakers improve passenger experience while meeting glare and thermal regulations. As a result, smart glazing is moving beyond a luxury feature and becoming an integrated functional component within modern vehicle architectures.

Automotive Smart Glass Market Trends Shaping Industry Demand

ADAS-Compatible Windshields Creating Functional Demand

One of the most visible automotive smart glass market trends is the integration of dimmable glass into ADAS-ready windshields. Heads-up displays require consistent visibility under changing light conditions, making selective dimming zones increasingly important. Smart glass allows HUD content to remain readable without darkening the full windshield, supporting driver focus and safety.

Panoramic Roof Adoption in Electric Vehicles

Electric vehicles are accelerating automotive smart glass market growth as manufacturers seek passive solutions to manage cabin heat and battery load. Large panoramic roofs equipped with smart glass reduce solar heat gain while preserving natural light, improving HVAC efficiency and driving range.

Regulatory Focus on Glare and UV Control

Stricter glare and ultraviolet exposure standards, especially in Europe, are pushing OEMs toward adaptive glazing solutions. Traditional tinted glass struggles to meet both visibility and UV requirements simultaneously. Smart glass solves this challenge by allowing on-demand tint adjustment, helping automakers standardize glazing designs across regions while remaining compliant. This regulatory alignment continues to strengthen the automotive smart glass market share across global platforms.

Automotive Smart Glass Market Segmentation

By Technology Type

-

Electrochromic glass

-

Suspended particle devices

-

Polymer dispersed liquid crystal

-

Thermo-chromic and photo-chromic variants

-

Hybrid and multi-stack solutions

By Application Type

-

Sunroof glass

-

Front and rear windshields

-

Rear and side windows

-

Smart HUD and display panels

By Vehicle Type

-

Passenger cars

-

Light commercial vehicles

-

Medium and heavy commercial vehicles

-

Buses and coaches

By Propulsion Type

-

Internal combustion engine vehicles

-

Electric vehicles

By Sales Channel

-

OEM installations

-

Aftermarket upgrades

By Geography

-

North America

-

United States

-

Canada

-

Rest of North America

-

South America

-

Brazil

-

Argentina

-

Rest of South America

-

Europe

-

Germany

-

United Kingdom

-

France

-

Italy

-

Spain

-

Russia

-

Rest of Europe

-

Asia-Pacific

-

China

-

Japan

-

South Korea

-

India

-

Indonesia

-

Vietnam

-

Philippines

-

Australia

-

Rest of Asia-Pacific

-

Middle East and Africa

-

United Arab Emirates

-

Saudi Arabia

-

Turkey

-

Egypt

-

South Africa

-

Rest of Middle East and Africa

Competitive Landscape of the Automotive Smart Glass Industry

The automotive smart glass industry remains moderately fragmented, with global glass manufacturers competing alongside specialized smart glazing developers. Competition increasingly centers on system integration, supply chain resilience, and long-term OEM partnerships rather than standalone material performance. Companies with vertically integrated manufacturing and localized production footprints maintain an advantage in large vehicle programs, while technology specialists focus on differentiated performance and licensing models.

Key Players in the Automotive Smart Glass Market

-

AGC Inc.

-

Saint-Gobain S.A.

-

Gentex Corporation

-

Nippon Sheet Glass Co. Ltd.

-

Corning Incorporated

Conclusion: Automotive Smart Glass Market

The automotive smart glass market is steadily transitioning from a premium comfort feature to a core vehicle system aligned with safety, efficiency, and design goals. Demand is reinforced by electric vehicle growth, panoramic roof integration, and increasing reliance on digital displays within the driver’s field of vision. While cost and aftermarket complexity remain considerations, ongoing scale benefits and module-based supply strategies are improving adoption economics.

As automakers seek differentiation without adding mechanical complexity, smart glass offers a practical balance of comfort, compliance, and functionality. With continued OEM investment and broader application coverage, the automotive smart glass market growth trajectory remains strong, positioning the sector for sustained expansion throughout the forecast period.