Next Generation Cancer Diagnostics Market Overview

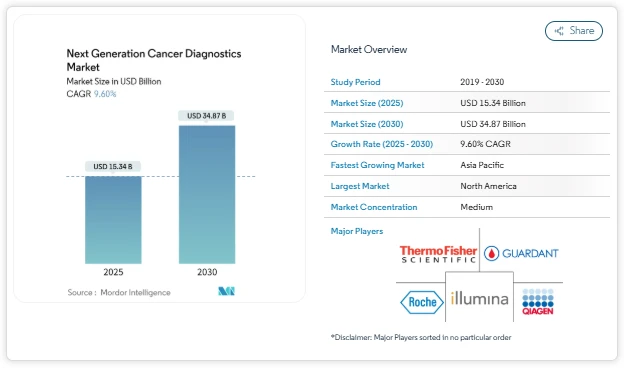

The next generation cancer diagnostics market size was valued at USD 15.34 billion in 2025 and is projected to reach USD 34.87 billion by 2030, growing at a CAGR of 9.6% during the forecast period. According to Mordor Intelligence, the next generation cancer diagnostics industry is witnessing consistent expansion as healthcare systems increasingly integrate genomic testing into routine oncology care.

The next generation cancer diagnostics market is being shaped by declining sequencing costs, improved analytical precision, and broader regulatory clarity around laboratory-developed tests and companion diagnostics. Hospitals and cancer centers are expanding in-house genomic testing capabilities, reducing turnaround times and improving treatment selection. As genomic profiling becomes part of standard oncology workflows, the next generation cancer diagnostics market share is widening across both developed and emerging healthcare systems.

Next Generation Cancer Diagnostics Market Trends Shaping the Industry

Declining Costs and Accuracy Improvements in NGS Platforms

One of the most important next generation cancer diagnostics market trends is the continued reduction in next-generation sequencing costs. Lower instrument and reagent expenses are enabling community hospitals and regional laboratories to adopt comprehensive tumor profiling.

Growing Adoption of Liquid Biopsy for Treatment Guidance

Liquid biopsy is becoming a key contributor to next generation cancer diagnostics market growth. Circulating tumor DNA assays are increasingly used for therapy selection and treatment monitoring, particularly when tissue samples are difficult to obtain. The ability to track tumor evolution through minimally invasive testing supports personalized care and improves patient experience.

Expansion of Companion Diagnostics in Targeted Oncology

The growing alignment between pharmaceutical companies and diagnostic developers is another defining next generation cancer diagnostics market trend. Companion diagnostics are increasingly developed alongside targeted therapies to identify eligible patient populations.

Next Generation Cancer Diagnostics Market Segmentation Analysis

By Technology

-

Next-Generation Sequencing (NGS)

-

qPCR and Multiplexing

-

Lab-on-a-Chip and RT-PCR

-

Circulating Tumor DNA Assays

-

Protein Microarrays

-

DNA Microarrays

-

Other Multi-Omics Platforms

By Cancer Type

-

Breast Cancer

-

Lung Cancer

-

Colorectal Cancer

-

Prostate Cancer

-

Other Cancers

By End User

-

Reference Laboratories

-

Hospital and Cancer Centres

-

Academic and Research Institutes

-

Pharmaceutical and Biotech Companies

-

CROs and Others

By Geography

-

North America

-

Europe

-

Asia Pacific

-

Middle East and Africa

-

South America

Next Generation Cancer Diagnostics Market Key Players and Competitive Landscape

The next generation cancer diagnostics industry remains moderately fragmented, with global platform providers and specialized diagnostics companies competing across technologies and regions.

Key players include:

-

Roche Diagnostics

-

Illumina

-

Thermo Fisher Scientific

-

Guardant Health

-

QIAGEN

Conclusion:

The next generation cancer diagnostics market is positioned for sustained expansion as precision oncology becomes central to cancer management strategies. Declining sequencing costs, expanding liquid biopsy applications, and stronger integration of companion diagnostics are reinforcing long-term next generation cancer diagnostics market growth.

Regional screening initiatives, regulatory clarity, and growing clinician familiarity with genomic testing are expected to strengthen the next generation cancer diagnostics market forecast over the coming years. While reimbursement variability and regulatory complexity remain considerations, the overall direction of the next generation cancer diagnostics industry reflects steady adoption across hospitals, research institutions, and pharmaceutical pipelines.