Introduction to the Oil Refining Market

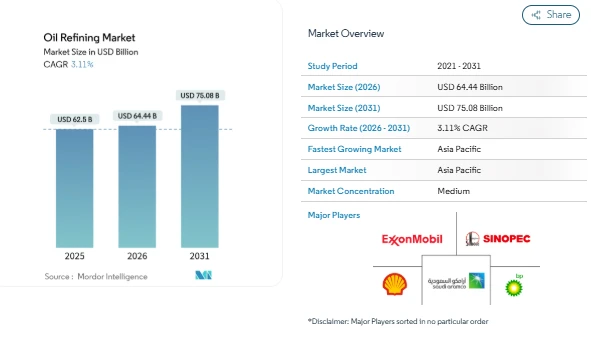

The global Oil Refining Market is witnessing steady growth as refiners navigate shifting fuel demands and expanding petrochemical opportunities. The market was valued at USD 62.5 billion in 2025 and is projected to grow to USD 75.08 billion by 2031, at a CAGR of over 3% during the forecast period. This growth is supported by advancements in refinery integration, desulfurization upgrades, and the development of renewable diesel platforms.

The Oil Refining Market Size is expanding as operators diversify fuel slates, optimize conversion processes, and adapt to regional regulatory frameworks. With crude flexibility and petrochemical integration becoming key differentiators, the Oil Refining Industry is evolving to balance profitability with sustainability imperatives.

Trends & Developments in the Oil Refining Market

-

Petrochemical Feedstock Expansion in Asia: Refiners in China, India, and Southeast Asia are increasingly integrating catalytic crackers, polypropylene, and naphtha processing units to capture higher-margin chemical products. Projects like CNOOC’s Ningbo expansion illustrate how investment in polymers boosts crude throughput while mitigating gasoline demand pressures.

-

Desulfurization Retrofits for Low-Sulfur Fuels: Post-IMO 2020 regulations have accelerated investments in hydrodesulfurization units and premium bunker fuel production. These upgrades support Oil Refining Market Growth by increasing product flexibility and maintaining compliance with global fuel standards.

-

National Oil Companies Leading Integration: NOCs such as Saudi Aramco and ADNOC are leveraging crude production advantages to develop integrated complexes, combining refining and chemical assets. These models strengthen export potential, optimize margins, and shape regional Oil Refining Market Share dynamics.

-

U.S. Light Tight Oil Boom: Shale output growth has prompted investments in condensate splitters and flexible processing units, enhancing light crude utilization for gasoline and petrochemical feedstocks. Projects by Phillips 66 and Verde Clean Fuels demonstrate the impact of regional feedstock abundance on global market positioning.

Market Breakdown Segmentation of the Oil Refining Market

-

By Product Slate:

-

Light Distillates (Gasoline, Naphtha)

-

Middle Distillates (Diesel/Gasoil, Jet/Kero)

-

Fuel Oil and Residuals

-

Petrochemical Feedstocks (Propylene, Aromatics)

-

By Ownership:

-

National Oil Companies (NOCs)

-

Integrated Oil Companies (IOCs)

-

Independent/Merchant Refiners

-

By Geography:

-

North America (United States, Canada, Mexico)

-

Europe (United Kingdom, Germany, France, Spain, Nordic Countries, Russia, Rest of Europe)

-

Asia-Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Indonesia, Vietnam, Australia, Rest of Asia-Pacific)

-

South America (Brazil, Argentina, Colombia, Rest of South America)

-

Middle East & Africa (United Arab Emirates, Saudi Arabia, South Africa, Egypt, Rest of Middle East & Africa)

Key Players in the Oil Refining Market

-

Sinopec Corp.

-

Exxon Mobil Corporation

-

Saudi Aramco (including JV capacity)

-

Shell plc

-

BP plc

Conclusion

The Oil Refining Market Forecast indicates steady growth driven by strategic upgrades, regional expansion, and petrochemical integration. Asia-Pacific, the Middle East, and select African markets are leading throughput expansion, while OECD regions focus on efficiency, rationalization, and sustainable platform transitions.

Operators with diversified fuel slates, flexible conversion units, and access to integrated chemical production are positioned to capture the largest share of the Oil Refining Market Size. As crude availability, regulatory compliance, and petrochemical demand continue to influence operations, the Oil Refining Market is set to expand steadily over the next decade, providing balanced growth opportunities across geography, product types, and ownership structures.