Introduction to the China Renewable Energy Market

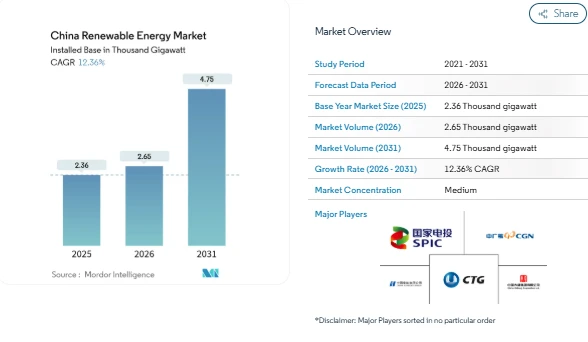

The China Renewable Energy Market is witnessing remarkable growth, reflecting the country's commitment to clean energy and carbon neutrality. In 2026, the market size is projected to reach 2.65 thousand gigawatts, rising from 2.36 thousand gigawatts in 2025. By 2031, projections indicate the market could achieve 4.75 thousand gigawatts, with a compound annual growth rate (CAGR) of over 12%. This growth is fueled by a combination of government policies, declining costs of renewable technologies, and expanding private-sector participation.

China’s 2060 carbon neutrality pledge is driving growth in renewable energy, with state and private players investing in solar, wind, hydropower, and energy storage. Supportive policies, including the 14th Five-Year Plan, are helping the China Renewable Energy Market expand steadily, meeting both industrial and residential energy needs.

Growth Trends in the China Renewable Energy Market

Government Mandates and Policy Support

The central government has embedded decarbonization goals into legally binding capacity quotas, pushing provinces to accelerate renewable deployment. Industrial emitters are also incentivized to adopt renewables through carbon-trading pilots and mandatory environmental reporting, ensuring long-term demand stability for the China Renewable Energy Market.

Declining Costs for Solar and Wind

Utility-scale solar power now delivers electricity at costs below conventional coal-fired energy in many provinces. Falling polysilicon prices and efficient manufacturing techniques allow solar modules to cost under USD 0.10 per watt. Wind energy costs have similarly dropped due to larger turbines and improved installation practices. The cost advantage has led to more renewable projects being approved, supporting overall China Renewable Energy Market Trends.

Growth in Hybrid Renewable-Storage Projects

Energy-storage adoption is growing rapidly, with installed capacity exceeding 70 GW by 2024. Grid codes require storage integration in curtailment-prone regions, prompting developers to pair solar and wind projects with lithium-ion systems. Storage not only helps balance grid supply but also earns additional revenue through ancillary services, strengthening the financial case for renewable projects in the China Renewable Energy Industry.

Market Segmentation in the China Renewable Energy Market

By Technology:

-

Solar Energy – Largest segment, representing nearly half of total installed capacity. Falling module costs and utility-scale projects support growth.

-

Wind Energy – Onshore and offshore projects contribute about one-third of capacity, with offshore wind and deep-water turbines expanding potential.

-

Hydropower – Includes both large and small dams, plus pumped-storage projects, providing grid flexibility.

-

Bioenergy and Geothermal – Support niche and distributed applications.

-

Ocean Energy – Emerging segment with tidal and wave energy pilots achieving high capacity factors.

By End-User:

-

Utilities – Dominate 82% of installed capacity due to preferential grid access and financing.

-

Commercial & Industrial – Growing rapidly via rooftop solar, captive generation, and PPAs.

-

Residential – Modest adoption but gradually increasing with incentives and low-interest loans.

By Geography:

-

Eastern Coastal Provinces – Absorb the largest share of generation; expanding offshore wind and rooftop solar.

-

Northwest Regions – Ideal for utility-scale solar and wind projects but face curtailment challenges.

-

Southwest Provinces – Focus on hydropower and integrated solar-hydro-wind systems.

Key Players in the China Renewable Energy Market

-

China Three Gorges Corporation – Leading hydropower developer with growing wind and solar investments.

-

State Power Investment Corporation (SPIC) – Involved in large-scale wind, solar, and storage projects.

-

China Huaneng Group – Active across multiple renewable technologies and energy-storage integration.

-

China Datang Corp Renewable Power – Focused on diversified renewable assets and grid-scale solutions.

-

China General Nuclear New Energy – Invests in solar, wind, and offshore energy projects.

Conclusion

The China Renewable Energy Market is set for strong growth, supported by government policies, declining technology costs, and increasing adoption by corporate and industrial users. Solar and wind remain the dominant segments, while emerging areas like ocean energy and energy storage are creating new opportunities. Improvements in transmission, grid integration, and supply-chain stability are helping the market operate more efficiently.