Introduction to the Plastics Injection Molding Market

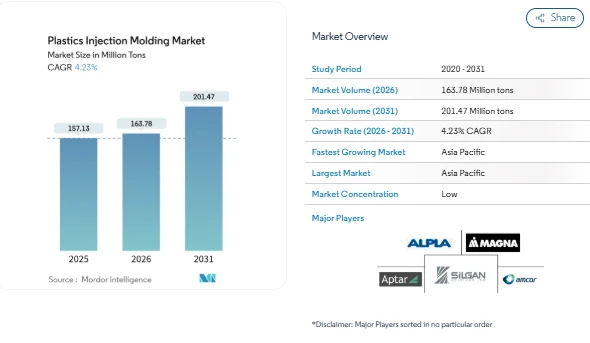

The Plastics Injection Molding Market is witnessing steady growth, with the global market size projected to increase from 163.78 million tons in 2026 to 201.47 million tons by 2031, representing a CAGR of 4.23%. This growth reflects the market’s critical role in producing cost-effective, high-volume components for diverse industries such as packaging, automotive, electronics, and healthcare. Rising e-commerce, expanding electric vehicle (EV) production, and stricter recyclability regulations are driving demand across various sectors.

Market Drivers & Insights in the Plastics Injection Molding Market

Surge in E-commerce-Driven Packaging Demand

The expansion of e-commerce has created strong demand for lightweight yet durable packaging solutions. Companies increasingly prefer mono-material polyethylene and polypropylene packaging that reduces material usage while maintaining strength. These trends are increasing throughput and supporting growth in thin-wall container and closure segments, forming a significant portion of the Plastics Injection Molding Market.

Lightweighting Requirements in Automotive and EVs

Automakers are replacing metal components with injection-molded plastics to meet CO₂ emission targets and enhance EV efficiency. Thermoplastic battery housings with flame-retardant walls are replacing steel alternatives, reducing vehicle weight. High-performance polymers like polyamide, polycarbonate, and recycled polypropylene are increasingly used in interior and exterior trims.

Growing Need for Single-Use Medical Disposables

Healthcare facilities are standardizing on single-use medical devices, including syringes, pipettes, and diagnostic cartridges. This surge in demand has prompted expansions in ISO 13485-certified molding capacity. Equipment advancements, such as multi-cavity injection systems, allow rapid production cycles while maintaining precision. High-performance resins, like cyclic olefin copolymer, offer chemical inertness and optical clarity, reinforcing the market’s premium segment in medical applications.

Market Categorization in the Plastics Injection Molding Industry

By Raw Material Type

-

Polypropylene

-

Acrylonitrile Butadiene Styrene (ABS)

-

Polystyrene

-

Polyethylene

-

Polyvinyl Chloride (PVC)

-

Polycarbonate

-

Polyamide

-

Other Raw Materials

By Application

-

Packaging

-

Building and Construction

-

Consumer Goods

-

Electronics

-

Automotive and Transportation

-

Healthcare

-

Other Applications

By Geography

-

Asia-Pacific

-

China

-

India

-

Japan

-

South Korea

-

Rest of Asia-Pacific

-

North America

-

United States

-

Canada

-

Mexico

-

Europe

-

Germany

-

United Kingdom

-

France

-

Italy

-

Russia

-

Rest of Europe

-

South America

-

Brazil

-

Argentina

-

Rest of South America

-

Middle-East and Africa

-

Saudi Arabia

-

South Africa

-

Rest of Middle-East and Africa

Key Players in the Plastics Injection Molding Market

-

ALPLA – specializes in packaging solutions and lightweight injection molding.

-

Amcor PLC – global leader in flexible and rigid packaging.

-

AptarGroup, Inc. – provides precision closures and dispensing systems.

-

Magna International Inc. – automotive trims and components supplier.

-

Silgan Holdings Inc. – focuses on food packaging and closures.

Conclusion

The Plastics Injection Molding Market is poised for steady growth through 2031, driven by increasing packaging demand, automotive lightweighting, and healthcare applications. Asia-Pacific remains a key growth region, while North America and Europe focus on reshoring and sustainability. Market segmentation by raw materials, applications, and geography highlights opportunities for diversified investments. Regulatory mandates and volatile resin pricing present challenges but also foster sustainable practices.