Introduction to the Agricultural Machinery Market

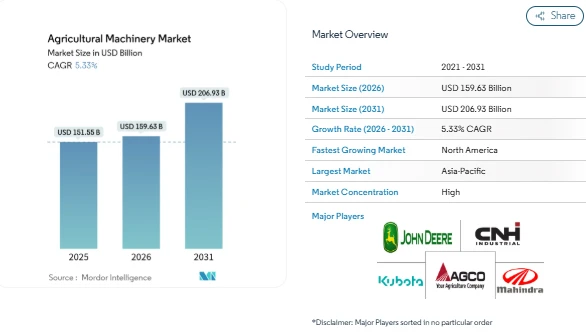

The Agricultural Machinery Market has emerged as a critical sector driving efficiency and productivity in the global farming landscape. Valued at USD 151.55 billion in 2025, the market is projected to grow from USD 159.63 billion in 2026 to reach USD 206.93 billion by 2031, registering a CAGR of 5.33% during the forecast period. The growth of this market is fueled by increasing demand for mechanized solutions to address labor shortages, optimize farm yields, and adopt precision agriculture practices.

Farmers and agribusinesses are increasingly leveraging these tools to improve operational efficiency, reduce input costs, and meet regulatory requirements linked to sustainability and climate-friendly practices. This trajectory underlines the importance of understanding Agricultural Machinery Market Trends, segmentation, and competitive dynamics to anticipate future growth opportunities.

Key Trends in the Agricultural Machinery Market

Precision Agriculture and Connected Platforms:

The shift from purely mechanical machinery to sensor-enabled, data-driven platforms is transforming farm operations. Equipment now collects telemetry, yield maps, and soil data, which feed algorithms that optimize planting, irrigation, and harvesting. These innovations not only improve output but also create recurring revenue opportunities for manufacturers through software subscriptions and predictive maintenance services.

Government Incentives and Subsidies:

National and regional programs significantly influence Agricultural Machinery Market Growth. In countries like India, equipment subsidies cover up to half of the purchase cost, while U.S. programs like the Environmental Quality Incentives Program allocate substantial funding for climate-smart equipment. These incentives accelerate machinery adoption and encourage upgrades to newer, more efficient models.

Equipment-as-a-Service Models:

High upfront costs for advanced machinery have led to leasing and shared-service platforms. Service models like shared fleets allow smallholders to access modern tractors and harvesters without heavy capital investment, expanding market reach and encouraging intensive utilization of machinery.

Market Segmentation of Agricultural Machinery

-

By Type

-

Tractors

-

Horsepower:

-

Less than 40 HP

-

40 HP–99 HP

-

Greater than 100 HP

-

Tractor Type:

-

Compact Utility Tractors

-

Utility Tractors

-

Row-Crop Tractors

-

Plowing and Cultivating Machinery

-

Plows

-

Harrows

-

Cultivators and Tillers

-

Other Plowing and Cultivating Machinery

-

Planting Machinery

-

Seed Drills

-

Planters

-

Spreaders

-

Other Planting Machinery

-

Harvesting Machinery

-

Combine Harvesters–Threshers

-

Forage Harvesters

-

Other Harvesting Machinery

-

Haying and Forage Machinery

-

Mower-conditioners

-

Balers

-

Other Haying and Forage Machinery

-

Irrigation Machinery

-

Sprinkler Irrigation

-

Drip Irrigation

-

Other Irrigation Machinery

-

Other Types

-

By Geography

-

North America

-

United States

-

Canada

-

Mexico

-

Rest of North America

-

Europe

-

Germany

-

France

-

United Kingdom

-

Russia

-

Rest of Europe

-

Asia-Pacific

-

China

-

India

-

Japan

-

Australia

-

Rest of Asia-Pacific

-

South America

-

Brazil

-

Argentina

-

Rest of South America

-

Middle East

-

Saudi Arabia

-

United Arab Emirates

-

Rest of Middle East

-

Africa

-

South Africa

-

Nigeria

-

Rest of Africa

Key Players in the Agricultural Machinery Market

-

Deere & Company: Leads in precision agriculture technologies and autonomous tractors, offering end-to-end digital agronomy solutions.

-

AGCO Corporation: Focuses on connected equipment, hybrid drivetrains, and sustainable machinery across multiple regions.

-

Kubota Corporation: Specializes in compact tractors and horticultural machinery, catering to small-scale farms and fragmented land holdings.

-

CNH Industrial N.V.: Strengthens its presence through acquisitions and local manufacturing, addressing supply chain efficiency in North America and Europe.

-

Mahindra & Mahindra Limited: Emphasizes affordability and entry-level mechanization solutions, particularly in emerging markets.

Conclusion

The Agricultural Machinery Market continues to grow as farmers seek solutions to labor shortages, enhance productivity, and adopt precision farming practices. Mechanization, connected machinery, and equipment-as-a-service models are making advanced tools more accessible, while sustainability and low-emission requirements are shaping product development. Understanding key trends, market segments, and leading players is essential for stakeholders to navigate opportunities and support efficient, modern farming operations.