Automotive Semiconductor Market Overview

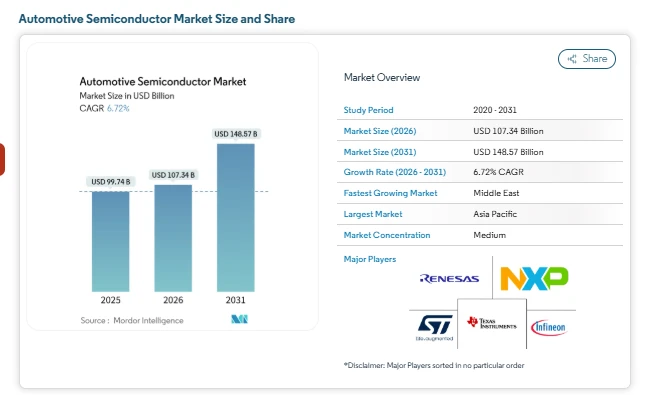

The automotive semiconductor market size is estimated at USD 107.34 billion in 2026 and is expected to reach USD 148.57 billion by 2031, registering a CAGR of 6.72% during 2026–2031. The industry continues to expand as vehicles integrate higher levels of electrification, connectivity, and safety functionality. Increasing semiconductor content per vehicle has become a defining factor behind market growth, especially as battery electric vehicles carry significantly higher chip value compared to internal combustion engine models. Emerging investments in the Middle East and other developing regions are also contributing to market growth by encouraging localized assembly and advanced safety integration.

The market forecast indicates that value expansion is being driven more by chip intensity per vehicle than by overall vehicle production volumes. Zonal electrical and electronic architectures are reducing the number of individual control units while increasing demand for high-performance system-on-chip platforms. At the same time, regulatory mandates for advanced driver-assistance systems are strengthening the long-term market share of safety-focused suppliers. Asia Pacific currently leads global revenue, supported by strong electric vehicle production and semiconductor manufacturing ecosystems.

Key Automotive Semiconductor Market Growth Drivers

Electrification Increasing Chip Content

Electrification remains a central automotive semiconductor market trend. Battery electric vehicles require traction inverters, onboard chargers, battery management systems, and high-voltage power electronics. This significantly increases semiconductor value compared to combustion models. Silicon carbide devices are increasingly used in power modules for improved efficiency and faster charging. Automakers are also signing long-term agreements to secure wide-bandgap semiconductor supply, reflecting how electrification directly supports automotive semiconductor market growth. Hybrid vehicles also contribute, as dual power management systems raise chip requirements.

Rising Demand for ADAS and Safety Systems

Safety regulations across major markets are standardizing advanced driver-assistance systems in mainstream vehicles. Features such as automated emergency braking, intelligent speed assistance, lane-keeping support, and driver monitoring require radar, camera modules, and high-performance processors. As governments expand mandatory safety features, semiconductor bill-of-materials per vehicle rises. This trend strengthens automotive semiconductor market share for suppliers with certified functional safety expertise. It also reinforces the long-term automotive semiconductor market forecast as safety content becomes standard even in entry-level vehicles.

Zonal E/E Architectures and Software-Defined Vehicles

Automakers are transitioning toward zonal electrical and electronic architectures. Instead of dozens of distributed control units, vehicles now rely on centralized computing platforms. This shift is reshaping automotive semiconductor industry demand toward advanced processors, high-speed connectivity chips, and secure memory solutions. Software-defined vehicles require over-the-air update capability and hardware security modules. As a result, integrated circuits and system-on-chip platforms are gaining importance, directly influencing the market size across premium and mass-market segments.

Supply Chain Localization and Capacity Expansion

Persistent chip shortages have encouraged regional diversification of semiconductor production. Governments are supporting domestic fabrication and packaging facilities to reduce dependency on imports. This supply realignment affects automotive semiconductor market trends and patterns, as qualification cycles and sourcing strategies evolve. Although lead times remain elevated compared to historical levels, new investments in mature-node capacity aim to stabilize supply over the market forecast period.

Check out more details and stay updated with the latest industry trends, including the Japanese version for localized insights: https://www.mordorintelligence.com/ja/industry-reports/automotive-semiconductor-market?utm_source=globook

Automotive Semiconductor Market Segmentation

By Device Type

-

Discrete semiconductors

-

Optoelectronics

-

Sensors and microelectromechanical systems

-

Power modules

By Vehicle Propulsion

-

Internal combustion engine vehicles

-

Hybrid vehicles

-

Battery electric vehicles

-

Fuel cell vehicles

By Application

-

Powertrain and electrification

-

ADAS and autonomous driving

-

Body electronics

-

Infotainment and connectivity

By Business Model

-

Integrated Device Manufacturers (IDMs)

-

Fabless companies

-

Foundries

Automotive Semiconductor Industry Key Players

-

NXP Semiconductors N.V.

-

Infineon Technologies AG

-

Renesas Electronics Corporation

-

STMicroelectronics N.V.

-

Texas Instruments Inc.

Conclusion

The automotive semiconductor market trend is entering a phase where semiconductor value per vehicle matters more than total vehicle output. Electrification, mandated safety systems, and centralized computing architectures are collectively driving steady market growth. While supply chain constraints and high feature costs remain challenging, continued regional investment and technology adoption support a positive market forecast.

As electric vehicles expand their footprint and advanced driver-assistance systems become standard worldwide, the automotive semiconductor industry is expected to maintain consistent expansion throughout the forecast period. Overall, rising semiconductor intensity, diversified sourcing strategies, and the shift toward software-defined vehicles ensure that the market size will remain on an upward trajectory, supported by durable market trends across propulsion, safety, and computing domains