United States car loan Market Overview

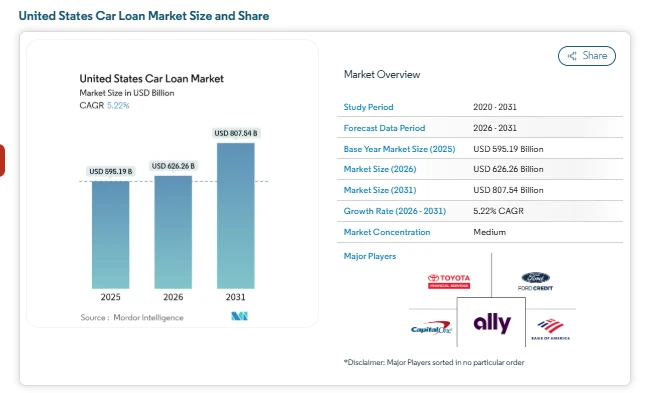

The United States car loan market size is projected to grow from USD 626.26 billion in 2026 to USD 807.54 billion by 2031, expanding at a CAGR of 5.22% during the forecast period. The market growth is supported by strong demand across passenger and used vehicle financing, increasing digital loan origination, and the expansion of captive lender programs. As lenders adopt AI-based underwriting and digital approval systems, processing efficiency is improving while broader borrower segments gain access to structured financing.

The industry is also influenced by federal and state-level electric vehicle incentives, which are helping lenders design tailored financing products. While the broader market faces pressures from interest rate levels and rising delinquencies in longer tenures, lenders are responding with tighter risk management and pricing discipline. The market forecast reflects a balanced outlook shaped by demand resilience, digital transformation, and regulatory oversight.

Key United States car loan Market Growth Drivers

Rising Captive-Lender Penetration

Captive finance arms have regained strength as dealership inventories stabilized. This has supported the United States car loan market share of manufacturer-backed financing, especially in new vehicle purchases. Captives are leveraging internal vehicle and customer data to sharpen pricing and retention strategies. As promotional financing programs adjust with supply conditions, banks and credit unions are focusing on faster approval cycles instead of rate competition. This shift is redefining competitive positioning across the United States car loan industry.

Growth in EV Financing Incentives

Electric vehicle financing is becoming a defining theme in United States car loan market trends. Federal tax credits and state rebates are lowering effective borrowing costs for eligible buyers. Lenders are observing lower default probabilities among EV borrowers compared to traditional vehicle segments. However, volatility in used EV prices has led lenders to implement stricter loan-to-value controls. Risk models now consider battery health, mileage patterns, and resale conditions. This targeted approach supports sustainable United States car loan market growth while maintaining asset quality.

Digital Loan Origination Expansion

Digital transformation remains central to the United States car loan market forecast. End-to-end online workflows are now widely adopted, allowing borrowers to compare rates and secure approvals without visiting branches. AI-driven underwriting tools help lenders segment borrowers more precisely, improving approval accuracy and operational efficiency. Partnerships between dealerships, fintech firms, and traditional banks are accelerating digital penetration. Lenders that lack real-time decision tools at risk of losing share as consumers increasingly prefer seamless digital experiences.

Credit Union Shift Toward Indirect Lending

Credit unions are expanding dealer-originated lending channels to offset slower direct applications. Partnerships with fintech platforms allow them to reach near-prime borrowers while preserving cooperative pricing structures. This shift reflects broader United States car loan industry dynamics, where compliance standards and due diligence expectations are increasing. Technology investments are becoming necessary to remain competitive within the United States car loan market.

United States car loan Market Segmentation

By Vehicle Type

-

Passenger vehicles dominate overall volume.

-

Commercial vehicles require specialized underwriting models.

-

Data integration is improving risk precision across segments.

By Ownership

-

Used vehicles lead in overall share.

-

New vehicles depend on promotional financing programs.

-

Refinance activity supports portfolio optimization.

By Provider Type

-

Captive lenders dominate new vehicle funding.

-

Banks focus on relationship-driven lending.

-

Fintech players expand access through automated underwriting.

By Tenure

-

Less than three-year loans are gaining traction.

-

Three to five-year loans balance affordability and asset life.

-

Extended terms face tighter underwriting standards.

United States car loan Market Key Players

-

Ally Financial Inc.

-

Bank of America Corp.

-

Toyota Financial Services

-

Capital One Financial Corp.

-

Ford Motor Credit Co.

Explore more insights on United States car loan competitive landscape: https://www.mordorintelligence.com/industry-reports/united-states-car-loan-market/companies?utm_source=globbook

Conclusion

The market forecast indicates steady expansion supported by sustained financing demand, digital lending adoption, and EV-focused product innovation. While interest rate pressures and delinquency risks present challenges, lenders are actively adjusting underwriting frameworks and tenure structures to protect portfolio quality.

Passenger and used vehicle segments continue to anchor market size, while fintech-enabled platforms are influencing borrower expectations. As regulatory requirements evolve and data analytics become more advanced, competitive dynamics within the industry will increasingly favor institutions with integrated digital ecosystems. Overall, the United States car loan market growth trajectory remains positive through the forecast period, supported by disciplined lending practices, diversified provider participation, and targeted risk management strategies