Semiconductor Equipment Market Overview

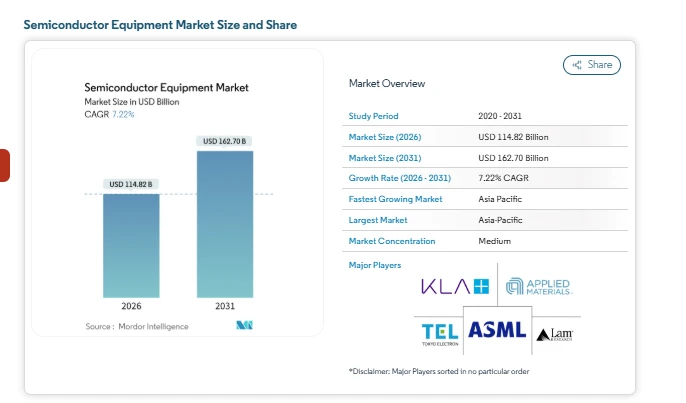

The global semiconductor equipment market is entering a new investment cycle driven by leading-edge logic, advanced packaging, and government-backed fabrication projects. According to industry analysis, the semiconductor equipment market size is estimated at USD 114.82 billion in 2026 and is projected to reach USD 162.70 billion by 2031, growing at a CAGR of 7.22% during 2026–2031.

This semiconductor equipment market growth reflects the shift toward infrastructure-focused chip production, where advanced nodes such as 2 nm, gate-all-around transistor architectures, and high-numerical-aperture extreme ultraviolet lithography tools are shaping capital spending priorities. At the same time, specialty packaging lines supporting chiplet designs are expanding the back-end segment of the semiconductor equipment industry. While advanced-node investments remain central to the semiconductor equipment market forecast, regional subsidy programs, export regulations, and specialty material supply constraints are also influencing shipment cycles and semiconductor equipment market share across regions.

Key Semiconductor Equipment Market Growth Drivers

Expansion of AI and Advanced Logic Capacity

Artificial intelligence workloads and data-center processors are driving demand for sub-5 nm manufacturing capacity. Advanced-node logic production requires more process steps and tighter inspection tolerances, increasing demand for metrology and inspection systems. Although mature nodes remain relevant for IoT and industrial applications, high-performance computing is strengthening the advanced equipment segment. This shift is a major contributor to semiconductor equipment market growth over the forecast period. One of the defining semiconductor equipment market trends is the migration from FinFET to gate-all-around transistor structures at advanced nodes.

Government Incentives and Fab Construction

Subsidy programs in major economies are accelerating fabrication plant construction. These incentives compress procurement cycles and bring forward tool purchases within the semiconductor equipment industry. Large-scale fab announcements across North America, Europe, and Asia-Pacific are reinforcing the semiconductor equipment market forecast through the mid-term horizon. However, industry participants are also assessing long-term utilization rates once subsidy cycles normalize. GAA devices require additional deposition and selective etch steps, increasing equipment intensity per wafer.

Rise of 3D Heterogeneous Integration

Advanced packaging is gaining attention as chiplet architectures become more common. Instead of relying only on die shrink, manufacturers are stacking and integrating multiple dies using hybrid bonding and wafer-level packaging technologies. This shift is strengthening the back-end segment of the semiconductor equipment market. Equipment such as precision bonders, wafer-level fan-out systems, and advanced test platforms are seeing steady demand. Over time, this could gradually rebalance semiconductor equipment market share between front-end and back-end categories. High-NA EUV lithography systems are also being introduced for advanced patterning. These systems demand upgraded facilities, vibration control, and thermal stability

Export Controls and Regional Realignment

Export restrictions on advanced lithography and etch systems are influencing regional semiconductor equipment market growth patterns. Shipments of leading-edge tools are increasingly concentrated in allied regions, while domestic equipment suppliers in restricted markets are expanding their role in mature-node production. This bifurcation is shaping competitive positioning within the broader semiconductor equipment industry and influencing long-term semiconductor equipment market trends.

Check out more details and stay updated with the latest industry trends, including the Japanese version for localized insights: https://www.mordorintelligence.com/ja/industry-reports/semiconductor-equipment-market?utm_source=globbook

Semiconductor Equipment Market Segmentation

By Equipment Type

-

Front-End Equipment

-

Lithography

-

Etch

-

Deposition

-

Metrology and inspection

-

Back-End Equipment

-

Assembly and packaging

-

Bonding systems

-

Test equipment

By Supply-Chain Participant

-

Foundries

-

Integrated Device Manufacturers (IDMs)

-

OSAT Providers

By Wafer Size

-

300 mm wafers

-

200 mm wafers

-

Less than or equal to 150 mm wafers

By End-Use Industry

-

Computing and Data-Center

-

Communications

-

Automotive and Mobility

-

Consumer Electronics

-

Industrial and IoT

By Geography

-

Asia-Pacific

-

North America

-

Europe

-

Middle East & Africa and South America

Key Players in the Semiconductor Equipment Industry

-

ASML Holding NV

-

Applied Materials Inc.

-

Lam Research Corp.

-

Tokyo Electron Ltd.

-

KLA Corp.

Conclusion

The semiconductor equipment market is set for steady expansion through 2031, supported by advanced logic transitions, packaging complexity, and policy-driven fabrication investments. The projected semiconductor equipment market size and steady CAGR reflect continued capital intensity in both front-end and back-end manufacturing.

While high-NA EUV and GAA architectures anchor the leading edge of the semiconductor equipment industry, mature-node production and advanced packaging ensure diversified demand across segments. Export regulations and supply chain considerations may create regional differences, but overall semiconductor equipment market growth remains on track. As semiconductor design complexity increases and end-use industries from computing to automotive demand higher performance, the semiconductor equipment market forecast indicates sustained momentum, reinforcing the sector’s central role in the global semiconductor equipment industry