Introduction to the Europe Biochar Market

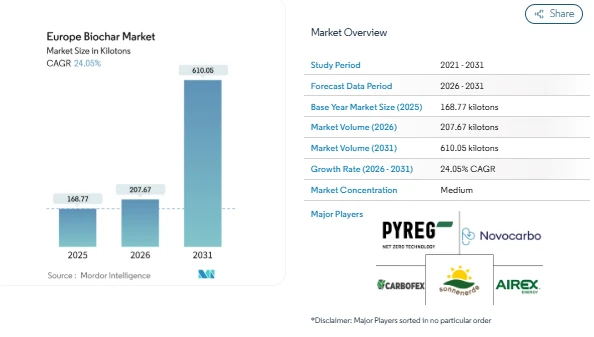

The Europe Biochar Market is experiencing a rapid surge, with its size estimated to grow from 207.67 kilotons in 2026 to 610.05 kilotons by 2031. This represents a compound annual growth rate of 24.05% over the forecast period. The market growth is driven by increasing adoption across agriculture, animal farming, and industrial applications, supported by policy incentives and carbon-credit initiatives.

The Europe Biochar Market is also influenced by the shift from experimental pilot projects to full-scale industrial deployment. Modular pyrolysis reactors that efficiently process forestry and agricultural residues are becoming the preferred technology. Additionally, applications in livestock feed, cement, steel, and phosphorus-rich municipal sludge are diversifying revenue streams while aligning with sustainability objectives.

Market Highlights in the Europe Biochar Market

-

Policy Support and Agricultural Demand: EU-funded programs under the Common Agricultural Policy, including Eco-Schemes, designate biochar as a subsidized soil amendment. France, Germany, and other countries have reported notable yield improvements in cereals and vineyards when biochar is applied, especially under drought conditions. Subsidies and demonstration projects accelerate adoption, although inconsistent application protocols and particle-size guidance create some variability in field outcomes.

-

Carbon-Credit Initiatives: Voluntary corporate buyers, including major technology and financial companies, are increasingly procuring biochar carbon removal certificates. Long-term agreements, such as NOVOCARBO’s 10-year municipal offtake contracts, provide financial certainty for producers, helping fund new plants. These deals also incentivize quality standards, including compliance with the European Biochar Certificate (EBC) audit requirements.

-

Inclusion under EU Fertilising Regulation (CMC14): With the transposition of CMC14, biochar that meets carbon and contaminant limits can circulate freely across EU countries. This has led to price premiums in early-adopter nations and encourages investments in traceability and certification.

Europe Biochar Market Division

Technology:

-

Pyrolysis

-

Gasification Systems

-

Other Technologies

Application:

-

Agriculture

-

Animal Farming

-

Industrial Uses

-

Other Applications

Geography:

-

Germany

-

United Kingdom

-

France

-

Italy

-

Spain

-

Nordic Countries

-

Turkey

-

Russia

-

Rest of Europe

Key Players in the Europe Biochar Market

-

PYREG GmbH: Manufactures modular pyrolysis reactors and provides toll-production services, securing both technology and feedstock reliability.

-

NOVOCARBO GmbH: Focuses on long-term municipal feedstock contracts and co-location with biomass power plants to stabilize production costs.

-

Carbofex Ltd: Partners with forestry and industrial sites to supply low-cost residues and optimize thermal efficiency.

-

Airex Energy and Sonnenerde GmbH: Serve niche applications and develop specialized biochar products for agricultural and industrial markets.

Conclusion

The Europe Biochar Market is set to grow steadily through 2031, fueled by rising demand in agriculture, animal farming, and industrial uses. Supportive policies, including EU carbon-removal mandates, CMC14 regulation, and Eco-Scheme subsidies, along with corporate carbon-credit agreements, are creating a favorable environment for producers.

Despite challenges like fragmented feedstock logistics and inconsistent pan-European agronomic guidance, opportunities in district-heating integration, industrial decarbonization, and soil amendment applications continue to expand. With sustained investments, regulatory support, and growing recognition of biochar’s environmental benefits, the Europe Biochar Market is expected to increase its market share and strengthen its industry presence across the continent.