Waste Recycling Services Market Overview

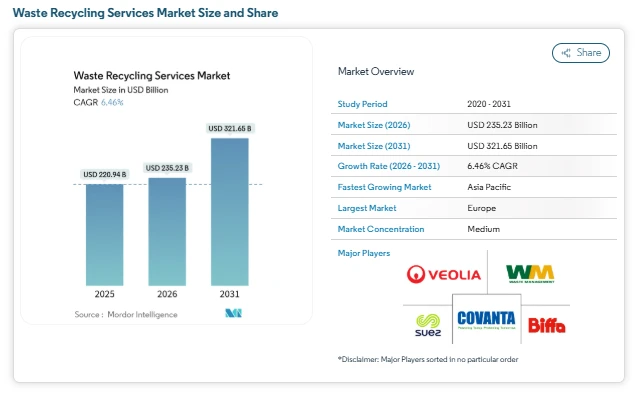

The waste recycling services market was valued at USD 220.94 billion in 2025 and is estimated at USD 235.23 billion in 2026, projected to reach USD 321.65 billion by 2031, registering a CAGR of 6.46%. This market growth reflects tightening Extended Producer Responsibility frameworks, increased corporate sustainability commitments, and modernization of sorting and processing infrastructure.

The expanding industry is being shaped by structured regulatory policies in Europe, growing lithium-ion battery recycling demand in Asia-Pacific and North America, and the digitalization of material recovery facilities. As regulatory clarity improves and corporate supply chains prioritize recycled inputs, the market size continues to expand across materials, end users, and geographies. Paper and paperboard remain central to overall market share, while battery recycling and chemical recycling processes are creating new revenue pockets.

Waste Recycling Services Market Trends

Extended Producer Responsibility Driving Market Contracts

The rollout of stricter Extended Producer Responsibility rules in Europe is accelerating long-term recycling contracts. Regulations require higher recycled content and improved recyclability in packaging formats, strengthening demand within the waste recycling services market. Harmonized compliance across European countries is benefiting integrated operators capable of handling cross-border logistics. Closed-loop programs in glass and plastic packaging are increasing contract stability, directly supporting waste recycling services market growth in the region.

Lithium-Ion Battery Recycling Expanding Specialized Services

The rapid rise in electric vehicle adoption is increasing battery waste volumes, especially in Asia-Pacific and North America. This shift is creating premium niches within the waste recycling services industry focused on safe recovery of lithium, cobalt, and nickel. Battery recycling involves advanced recovery techniques and strict safety protocols, raising entry barriers. As automakers secure long-term partnerships with recyclers, the waste recycling services market forecast indicates steady expansion in high-value metal recovery segments.

Corporate Net-Zero Commitments Supporting Closed-Loop Models

Major retailers and manufacturers are integrating recycled materials into procurement strategies. Waste diversion and circular sourcing are becoming procurement requirements, strengthening partnerships across the waste recycling services industry. Closed-loop recycling arrangements improve traceability and documentation. Operators that can certify emissions reduction and material origin are strengthening their waste recycling services market share, particularly in North America.

Digitalization of Sorting Facilities Improving Efficiency

Automation and robotics are increasingly deployed across OECD countries to improve capture rates and reduce labor risks. Digital monitoring systems improve material purity and reduce contamination. These operational upgrades are lowering long-term processing costs, improving margins, and supporting sustainable waste recycling services market growth. However, high upfront investment requirements are widening the gap between large integrated firms and smaller regional players in the waste recycling services market size

Commodity Price Volatility Impacting Profitability

Fluctuations in recycled commodity prices remain a challenge for the waste recycling services market. Revenue sensitivity to paper, plastic, and metal price swings influences short-term profitability. Larger firms mitigate this volatility through diversified portfolios and vertical integration, reinforcing consolidation trends across the waste recycling services industry. At the same time, secondary commodity price fluctuations and fire risks related to battery waste are influencing operational strategies within the industry. Packaging leads in market share due to regulated recycled content requirements. Electrical and electronics recycling is expanding steadily, supported by stricter cross-border waste movement rules

Waste Recycling Services Market Segmentation

By Material Type

-

Paper & Paperboard

-

Metals

-

Plastics

-

Glass

-

Batteries

-

Other Materials

By Source

-

Residential

-

Commercial

-

Industrial

-

Other Sources

By End-User Industry

-

Packaging

-

Automotive & Transportation

-

Electrical & Electronics

-

Healthcare

-

Construction

-

Other Industries

By Recycling Process

-

Mechanical Recycling

-

Chemical Recycling

-

Other Processes

By Geography

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East & Africa

Waste Recycling Services Market Key Players

-

Veolia Environnement S.A.

-

Waste Management, Inc.

-

SUEZ SA

-

Covanta Holding Corporation

-

Biffa plc

Conclusion

The waste recycling services market is entering a phase of structured, regulation-backed expansion. Clear policy frameworks, corporate circularity commitments, and specialized recycling niches are supporting predictable market growth. Although price volatility and safety risks remain concerns, long-term contracts and integrated service models are improving revenue stability across the industry.

Looking ahead, the waste recycling services market forecast remains positive through 2031, supported by regulatory enforcement, battery waste recovery demand, and increased adoption of chemical recycling solutions. As sustainability becomes embedded in procurement and manufacturing decisions, the market size and share are expected to strengthen steadily across regions and material segments.