Germany Furniture Market Outlook

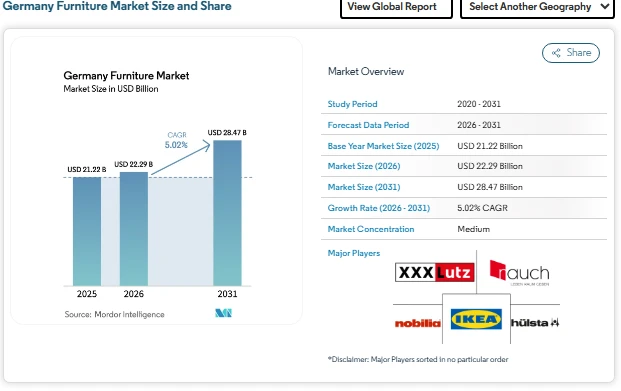

The Germany furniture market size in 2026 is estimated at USD 22.29 billion, rising from USD 21.22 billion in 2025 and projected to reach USD 28.47 billion by 2031, registering a CAGR of 5.02% during 2026–2031. The Germany furniture industry is currently navigating a period of cautious demand as consumers adjust spending due to inflation and higher living costs. This environment has led to softer sales across several categories, particularly in mid-range and economy segments, where discretionary purchases are more sensitive to household budgets.

Despite these pressures, the long-term market growth outlook remains steady. A potential easing of inflation and improvement in real wages could support a gradual recovery. Structural factors such as urban living, demographic changes, and the persistence of hybrid work arrangements continue to sustain demand for practical and adaptable furniture solutions. The Germany furniture market forecast therefore reflects both short-term caution and long-term stability, with manufacturers and retailers adjusting product portfolios to match evolving consumer priorities.

Germany Furniture Market Growth Drivers

Demand for Modular and Space-Efficient Solutions

Urbanization and smaller living spaces are driving interest in modular furniture that can adapt to changing household needs. Items that serve multiple functions or can be easily reconfigured are gaining traction, especially among younger consumers and city dwellers in the Germany furniture market growth. This shift is reinforcing the transition from bulky, permanent furniture toward flexible designs that support modern lifestyles.

Sustainability and Circular Design Requirements

Regulatory pressure from European sustainability policies, including the Ecodesign for Sustainable Products framework, is influencing production methods across the Germany furniture industry. Manufacturers are focusing on durable materials, repairable components, and recyclable designs. Sustainability is no longer a niche preference but a mainstream expectation, shaping purchasing decisions and brand positioning.

Aging Population and Healthcare Needs

Germany’s aging population is creating demand for specialized furniture designed for comfort, safety, and accessibility. Healthcare facilities assisted living centers, and home-care environments are investing in ergonomic beds, seating, and storage solutions. This segment is emerging as a stable contributor to Germany furniture market size, less affected by consumer spending cycles.

Hybrid Work and Home-Office Continuity

The shift toward flexible work arrangements continues to support demand for desks, ergonomic chairs, and storage units. Even as offices reopen, many households maintain dedicated workspaces at home. This sustained demand helps offset weakness in other residential categories and remains a defining Germany furniture market share.

Market Segmentation of the Germany Furniture Market

By Application

-

Home Furniture

-

Office Furniture

-

Hospitality Furniture

-

Educational Furniture

-

Healthcare Furniture

-

Other Applications

By Material

-

Wood

-

Metal

-

Plastic & Polymer

-

Other Materials

By Price Range

-

Economy

-

Mid-Range

-

Premium

By Distribution Channel

-

B2C/Retail

-

B2B/Project

By Geography

-

Southern Germany

-

Western Germany

-

Northern Germany

-

Eastern Germany

Key Players in the Germany Furniture Industry

-

IKEA

-

XXXLutz KG

-

Nobilia AB

-

Hülsta-Werke Hüls GmbH

-

Rauch Möbelwerke GmbH

Conclusion

The market is undergoing a transition shaped by economic caution and structural demand drivers. While inflation and living costs have restrained discretionary spending, long-term fundamentals such as demographic shifts, urban living patterns, and hybrid work continue to support steady demand. The Germany furniture market forecast suggests gradual recovery as consumer confidence improves and purchasing power stabilizes. Sustainability requirements are expected to play a central role in the future of the Germany furniture industry. Circular design principles, durable materials, and environmentally responsible production processes will likely become standard expectations rather than differentiators. Companies that adapt early to these requirements may strengthen their market share and build long-term customer trust. In summary, the market size reflects a stable yet evolving industry. Short-term challenges are balanced by long-term opportunities driven by sustainability, digitalization, and changing lifestyles. Companies that align their strategies with these trends will be best placed to succeed in the competitive Germany furniture industry landscape

Digital transformation is another decisive factor. Online retail channels are expanding rapidly, reshaping how consumers discover and purchase furniture. Retailers that combine physical showrooms with seamless digital experiences are better positioned to capture demand across different customer segments. This hybrid retail approach is likely to define market trends in the coming years. Additionally, specialized segments such as healthcare furniture and modular home solutions offer resilience against economic fluctuations. These categories address practical needs rather than purely decorative preferences, making them less vulnerable to downturns. As a result, they are expected to contribute meaningfully to overall market growth.