The X-Ray Imaging Devices Market segmentation framework, as detailed in this X-Ray Imaging Devices Market Report, provides a comprehensive and clinically structured view of the industry across five key dimensions: product type, portability, technology, application, and end user. This multi-dimensional segmentation enables stakeholders to identify the most commercially significant X-ray system categories, understand the clinical and operational drivers behind segment leadership, and align product development, capital investment, and market entry strategies with the highest-value growth opportunities across the X-ray imaging devices market. The market is valued at US$ 5,338.76 million in 2024 and is forecast to reach US$ 6,382.70 million by 2031 at a CAGR of 2.6%.

Request Sample Pages of this Research Study @ https://www.businessmarketinsights.com/sample/BMIPUB00031638

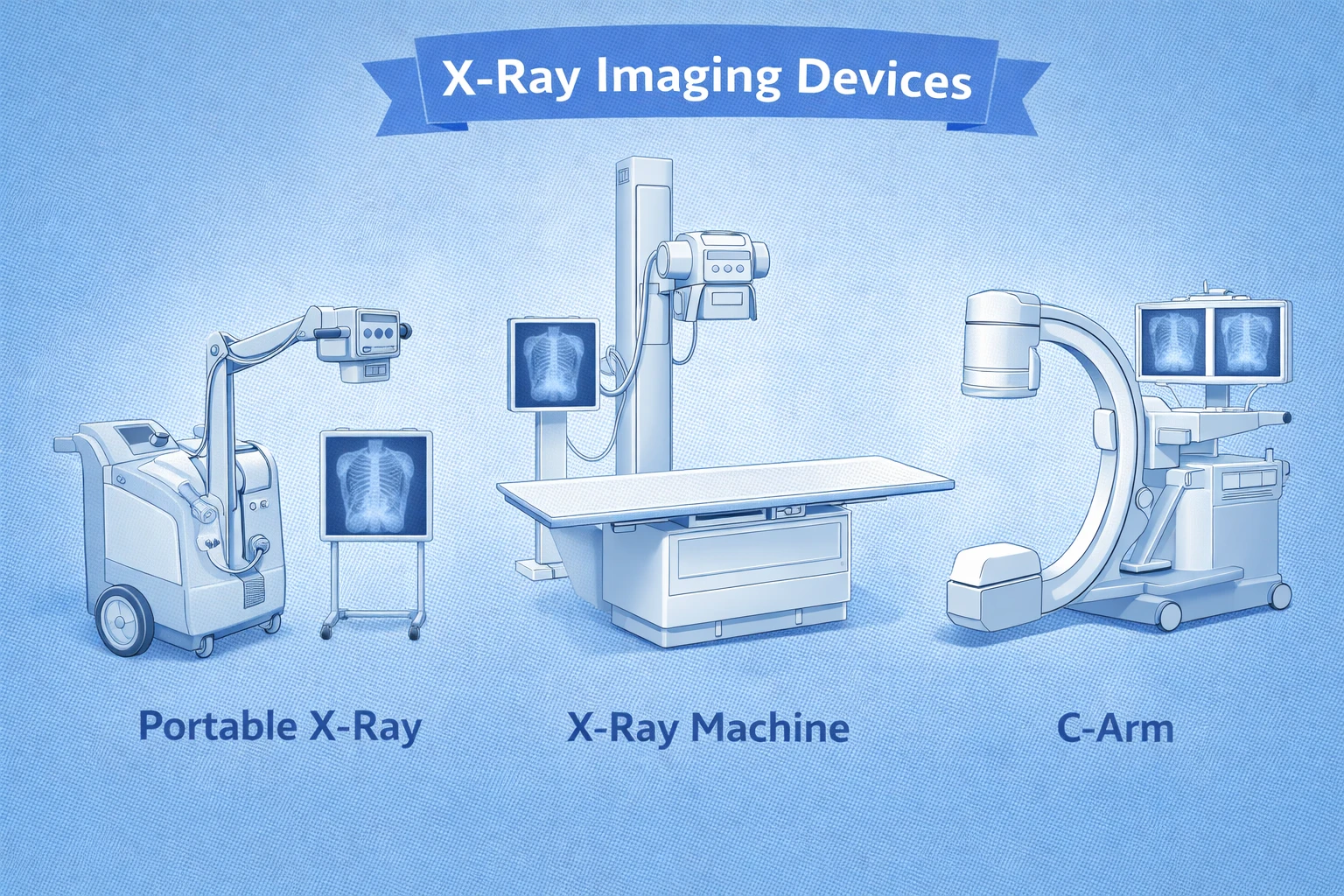

By Product Type

The product type segment encompasses conventional X-ray systems, digital X-ray systems, mobile X-ray systems, dental X-ray systems, mammography systems, and fluoroscopy systems. Digital X-ray systems dominated the market in 2024, driven by their faster imaging acquisition, superior image quality through flat panel detector technology, meaningfully lower radiation dose than analog film-screen systems, and seamless integration with hospital picture archiving and communication systems and electronic health records for efficient digital radiology workflows. NANO-X IMAGING's December 2024 FDA 510(k) clearance for the Nanox.ARC stationary X-ray system producing tomographic images for musculoskeletal, pulmonary, intra-abdominal, and paranasal sinus indications demonstrates breakthrough digital X-ray product innovation extending beyond two-dimensional projection radiography into three-dimensional tomographic acquisition capability. Mobile X-ray systems are the fastest-growing product segment, driven by bedside, ICU, and emergency department point-of-care imaging demand. Dental X-ray systems, mammography systems, and fluoroscopy systems each serve large and clinically important specialty-specific imaging markets.

By Portability

Stationary X-ray systems dominated the portability segment in 2024, serving as the backbone of hospital and diagnostic imaging center radiology departments with higher throughput, superior image quality, and compatibility with advanced imaging technologies for diverse clinical needs. Portable X-ray systems are the fastest-growing portability segment, driven by rising adoption in ICUs, emergency departments, rural healthcare facilities, and point-of-care settings where patient transport to stationary imaging suites is clinically impractical or logistically impossible.

By Technology

Direct radiography dominated the technology segment in 2024, preferred for real-time image acquisition with minimal processing time, high image clarity from flat panel detector direct conversion, and reduced repeat scan rates due to immediate image review capability. Computed radiography serves a transitional installed base between analog film and full digital direct radiography. Analog radiography represents a declining installed base in cost-sensitive markets.

By Application

General radiography led application revenues in 2024, encompassing chest, abdomen, skeletal, and trauma imaging across hospitals and outpatient settings. Orthopedic imaging, dental imaging, mammography, chest imaging, and fluoroscopy each contribute significant complementary application revenues.

By End User

Hospitals dominated end-user revenues with the highest X-ray procedure volumes across all specialties.

About Us

Business Market Insights is a one-stop industry research provider of actionable intelligence. Specializing in industries including Manufacturing and Construction, Semiconductor and Electronics, Healthcare, and more, the firm publishes over 500 research reports annually.

Contact Us

If you have any queries about this report or if you would like further information, please contact us: Phone: +16467917070 E-mail: sales@businessmarketinsights.com