Introduction to the Needle Coke Market

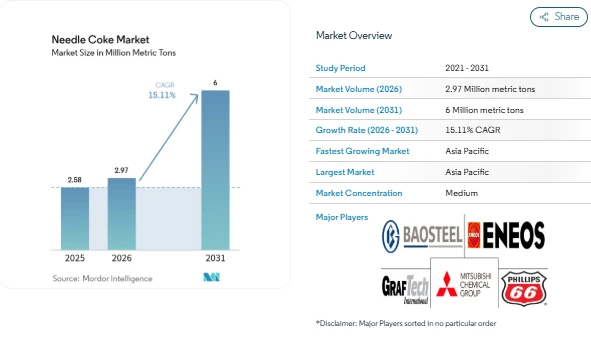

The Needle coke market is witnessing strong momentum as demand rises from both the steel and energy storage sectors. According to Mordor Intelligence, the Needle coke market size is expected to grow from 2.58 million metric tons in 2025 to 2.97 million metric tons in 2026, and further reach 6 million metric tons by 2031, registering a CAGR of 15.11% during the forecast period. This steady expansion reflects the increasing importance of needle coke in high-performance applications such as graphite electrodes and lithium-ion battery anodes.

The Needle coke industry is closely tied to structural changes in global manufacturing and energy systems. The shift toward electric arc furnace steel production and the scaling of battery manufacturing are creating consistent demand for high-purity carbon materials. At the same time, refinery improvements and integration strategies are helping stabilize supply, supporting overall Needle coke market growth.

Key Needle Coke Market Trends

Rising EAF Steel Capacity

One of the most important Needle coke market trends is the growing adoption of electric arc furnace steelmaking. This method relies heavily on graphite electrodes, which are made using needle coke. As more steel producers shift to this process due to environmental and cost considerations, demand for needle coke continues to rise. Scrap steel usage policies in major economies are also supporting this trend.

Expansion of Lithium-Ion Battery Production

Another major factor shaping the Needle coke market forecast is the rapid growth of lithium-ion battery manufacturing. Needle coke is a key raw material for synthetic graphite used in battery anodes. With electric vehicle production increasing globally, battery demand is rising, which directly supports the Needle coke market size. Even with some regional variations in supply, the need for high-purity materials keeps demand firm.

Refinery Integration and Feedstock Stability

Refinery upgrades are improving the availability of low-sulfur feedstock used to produce high-quality needle coke. Integrated operations allow companies to control raw material supply and manage costs more effectively. This trend is strengthening the overall Needle coke market share of petroleum-based products.

Needle Coke Market Segmentation Overview

-

By Product Type

-

Petroleum-Based Needle Coke

-

Coal-Tar Pitch-Based Needle Coke

-

By Application

-

Graphite Electrodes

-

Lithium-Ion Batteries

-

Other Applications

-

By Geography

-

Asia-Pacific

-

North America

-

Europe

-

South America

-

Middle East and Africa

Leading Companies in the Needle Coke Market

-

China Baowu Steel Group Corp., Ltd.

-

China National Petroleum Corporation

-

ENEOS Corporation

-

GrafTech International

-

Indian Oil Corporation

-

Mitsubishi Chemical Group Corporation

-

Nippon Steel Corporation

-

PetroChina

-

Phillips 66 Company

-

POSCO Future M

-

Shandong Yida New Materials Co., Ltd.

-

Shanxi Hongte Coal Chemical Co Ltd

-

Sinopec

-

Tokai Carbon Co., Ltd.

Conclusion

The Needle coke market is set for steady expansion, supported by strong demand from both traditional and emerging sectors. The continued shift toward electric arc furnace steelmaking and the rapid scaling of lithium-ion battery production are key factors shaping the Needle coke market forecast. These drivers ensure that demand remains stable even as the market adjusts to regulatory and supply-side challenges.

Overall, the Needle coke market size is expected to grow steadily, with Asia-Pacific maintaining a dominant position while other regions gradually expand their presence. The balance between supply, regulation, and end-use demand will continue to define the direction of the Needle coke market trends in the coming years.