Dashboard Camera Market Overview

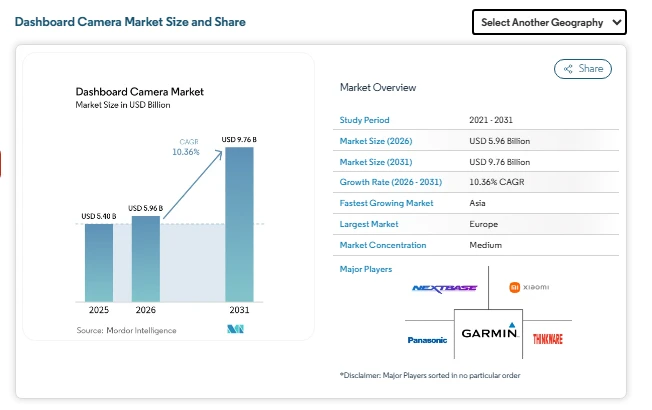

The global dashboard camera market size was valued at USD 5.40 billion in 2025 and is estimated to grow from USD 5.96 billion in 2026 to reach USD 9.76 billion by 2031, registering a CAGR of 10.36% during the forecast period. The steady rise in the market size reflects increasing demand for in-vehicle video recording solutions across private vehicles, commercial fleets, and public transport systems. As road safety concerns intensify and accident disputes become more common, dashboard cameras are being viewed as practical tools for documentation, driver accountability, and insurance validation.

Government mandates and policy frameworks in several regions are encouraging adoption of event data recorders and video monitoring systems. At the same time, insurers are integrating video evidence into telematics programs to streamline claims processing and reduce fraud. These factors collectively support dashboard camera market growth across developed and emerging economies alike. Consumer awareness is also playing a major role. Drivers increasingly prefer devices that provide real-time recording, parking surveillance, and emergency capture features. The integration of artificial intelligence, cloud storage, and mobile connectivity has expanded the functional scope of these products, improving perceived value. As a result, the dashboard camera industry is transitioning from a niche aftermarket accessory segment into a mainstream automotive electronics category with expanding dashboard camera market trends across regions.

Dashboard Camera Market Insights

Regulatory Support and OEM Adoption

Several European countries are promoting or mandating vehicle data recording systems to improve road safety and accident investigations. This supportive regulatory framework is encouraging automakers to install factory-fitted dashboard cameras as standard equipment. As a result, original equipment manufacturer (OEM) channels are becoming a key growth avenue. Such policies are strengthening long-term market prospects by embedding cameras directly into new vehicles.

Insurance Telematics and Fleet Benefits

Insurance companies, especially in North America, are integrating video-enabled telematics to enhance risk evaluation and speed up claims processing. Access to visual evidence helps reduce fraud and dispute resolution time. Commercial fleet operators benefit through lower insurance premiums and better monitoring of driver behavior. This trend is driving steady adoption of dashboard cameras across trucking, delivery, and passenger transport services.

Software Innovation and Connectivity

Competition in the industry is shifting from hardware specifications to advanced software capabilities. Features such as cloud storage, remote access, real-time alerts, and privacy-compliant data protection are becoming major differentiators. Buyers increasingly prefer systems that integrate seamlessly with smartphones and digital platforms. These software-driven functions are expanding the appeal of premium and connected camera solutions.

Fleet Monitoring and Durable Designs

Large transportation networks—including logistics firms, ride-hailing companies, and public transit agencies—are deploying multi-channel camera systems for safety and accountability. At the same time, manufacturers are improving durability to withstand extreme temperatures and harsh operating conditions. Heat-resistant components reduce maintenance costs and extend product lifespan, which is crucial for long-term fleet use. Together, reliability and monitoring capabilities are boosting global demand for advanced dashboard cameras.

Market Segmentation of the Dashboard Camera Market

By Technology

-

Basic

-

Advanced

-

Smart / AI-Integrated

By Product Type

-

Single-Channel

-

Dual-Channel

-

Rear-View / Surround

By Video Quality

-

SD and HD

-

Full-HD

-

4K / UHD

By Application

-

Personal Vehicles

-

Commercial Fleets

By Distribution Channel

-

In-store

-

Online

By Geography

-

North America

-

United States

-

Canada

-

Mexico

-

South America

-

Brazil

-

Argentina

-

Rest of South America

-

Europe

-

Germany

-

United Kingdom

-

France

-

Italy

-

Spain

-

Nordics (Sweden, Norway, Denmark, Finland)

-

Rest of Europe

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

ASEAN (Indonesia, Thailand, Malaysia, Vietnam, Philippines)

-

Rest of Asia Pacific

-

Middle East and Africa

-

Middle East

-

Saudi Arabia

-

United Arab Emirates

-

Turkey

-

Rest of Middle East

-

Africa

-

South Africa

-

Nigeria

-

Rest of Africa

Dashboard Camera Industry Leaders

-

Garmin Ltd.

-

Nextbase Ltd.

-

Thinkware Corporation

-

Panasonic Corporation

-

Xiaomi Corp.

Explore more insights on dashboard camera competitive landscape: https://www.mordorintelligence.com/industry-reports/dashboard-camera-market/companies?utm_source=globbook

Conclusion

The outlook for the market remains positive as safety awareness, regulatory initiatives, and digital connectivity continue to influence purchasing behavior. Increasing road congestion and accident rates are encouraging both individuals and organizations to adopt reliable recording solutions. In addition, the use of video evidence in legal and insurance processes is reinforcing the practical value of these devices. Fleet digitization is expected to remain a major driver for dashboard camera market growth. Transportation companies are investing in integrated monitoring systems that combine video, telematics, and analytics to improve efficiency and accountability. Meanwhile, consumer demand for smart vehicle accessories is supporting expansion in the retail aftermarket channel.

Regional dynamics will continue to shape the dashboard camera market forecast. Europe’s regulatory framework favors factory installation, North America emphasizes insurance-linked usage, and Asia benefits from large-scale vehicle production and growing middle-class car ownership. Together, these factors create a diversified demand base for the dashboard camera industry. Competition is intensifying as traditional aftermarket brands, telematics providers, and vehicle manufacturers compete within the connected mobility ecosystem. Partnerships, white-label manufacturing, and integrated software platforms are becoming common strategies to expand market reach. Companies that combine reliability, privacy compliance, and user-friendly features are likely to gain sustained dashboard camera market share