Automotive Head-Up Display Market Overview

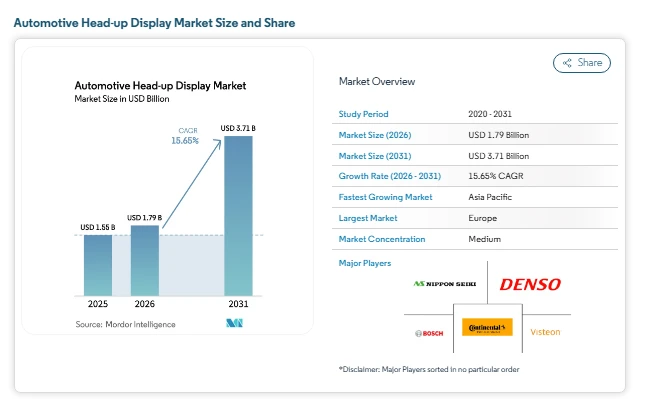

The automotive head up display market size was valued at USD 1.55 billion in 2025 and is estimated to grow to USD 1.79 billion in 2026, reaching USD 3.71 billion by 2031, registering a CAGR of 15.65% during the forecast period (2026–2031). This growth reflects the rising integration of advanced driver assistance systems and the shift toward connected and digital cockpits. The automotive head up display industry is evolving as manufacturers treat HUDs as a core interface rather than an optional feature.

These systems project essential driving data such as speed, navigation, and lane guidance directly into the driver’s line of sight, reducing the need to look away from the road. This functional advantage is influencing automotive head up display market growth across both premium and mid-range vehicles. Another key factor shaping the automotive head up display market forecast is cost reduction in optical components. As production scales and supply chains localize, HUD systems are becoming more accessible to a wider range of vehicles. This shift is also helping improve the automotive head up display market share across emerging regions, especially in Asia-Pacific.

Key Drivers in the Automotive Head-Up Display Market

Regulatory Push Supporting Automotive Head-Up Display Market Growth

Stricter safety regulations are playing a major role in the automotive head up display market trends. Europe’s General Safety Regulation II requires features such as intelligent speed assistance and lane-keeping alerts, increasing the need for clear and immediate driver information. HUD systems help meet these requirements by presenting data directly in the driver’s field of vision, reducing reaction time and improving safety compliance. Similar regulatory directions in North America further strengthen the automotive head up display industry outlook.

Premium Segment Driving Automotive Head-Up Display Market Size Expansion

Luxury vehicle manufacturers are redefining cabin design by placing digital displays at the center of user experience. In this segment, HUDs are no longer optional add-ons but standard features. Automakers are integrating larger projection areas and combining navigation with real-time driving data. This early adoption in premium vehicles supports automotive head up display market growth by spreading development costs and enabling faster entry into mid-range segments.

Cost Decline Improving Automotive Head-Up Display Market Share

The falling cost of picture generation units and optical systems is making HUD technology more viable for mass-market vehicles. Improved manufacturing efficiency and semiconductor scaling have lowered production expenses. This trend is expanding the automotive head up display market size by enabling broader adoption across vehicle categories, including commercial fleets. AR Integration Enhancing Automotive Head-Up Display Market Trends

Augmented reality is becoming a key differentiator in the automotive head up display industry. AR-enabled HUDs overlay navigation paths, hazard warnings, and lane guidance onto real-world views. With the support of cloud connectivity and faster data processing, these systems offer dynamic and context-aware information. This capability is influencing the automotive head up display market forecast by opening new revenue streams through software-based services.

Automotive Head-Up Display Market Segmentation

-

By HUD Type

-

Windshield HUD

-

Combiner HUD

-

By Technology

-

Conventional HUD

-

Augmented-Reality HUD

-

By Sales Channel

-

OEM-fitted

-

Aftermarket

-

By Vehicle Type

-

Passenger Cars

-

Commercial Vehicles

-

By Geography

-

North America

-

United States

-

Canada

-

Rest of North America

-

South America

-

Brazil

-

Argentina

-

Rest of South America

-

Europe

-

Germany

-

United Kingdom

-

France

-

Italy

-

Spain

-

Russia

-

Rest of Europe

-

Asia-Pacific

-

China

-

Japan

-

India

-

South Korea

-

Rest of Asia-Pacific

-

Middle East and Africa

-

United Arab Emirates

-

Saudi Arabia

-

Turkey

-

Egypt

-

South Africa

-

Rest of Middle East and Africa

Key Players in the Automotive Head-Up Display Market

The automotive head up display market share is largely held by established tier-one suppliers with strong manufacturing capabilities and global partnerships.

-

Continental AG

-

DENSO Corporation

-

Visteon Corporation

-

Robert Bosch GmbH

-

Nippon Seiki Co. Ltd

Conclusion

The automotive head up display market share is on a steady growth path supported by regulatory requirements, premium vehicle demand, and declining component costs. As HUD systems become a standard feature in modern vehicles, their role in improving driver awareness and safety continues to strengthen. This trend supports long-term automotive head up display market growth across regions and vehicle segments. The automotive head up display market forecast remains positive as automakers integrate more advanced features into their vehicles.

Augmented reality, connected services, and cloud-based rendering are expected to redefine how information is delivered to drivers. These developments will further expand the automotive head up display market size and create new opportunities within the automotive head up display industry. Overall, the automotive head up display market is transitioning from a niche technology to a widely adopted solution. With continued improvements in cost efficiency and functionality, the automotive head up display market share is expected to increase steadily, making HUD systems an essential component of future vehicle design