Data Center Market Size and Forecast (2025–2033)

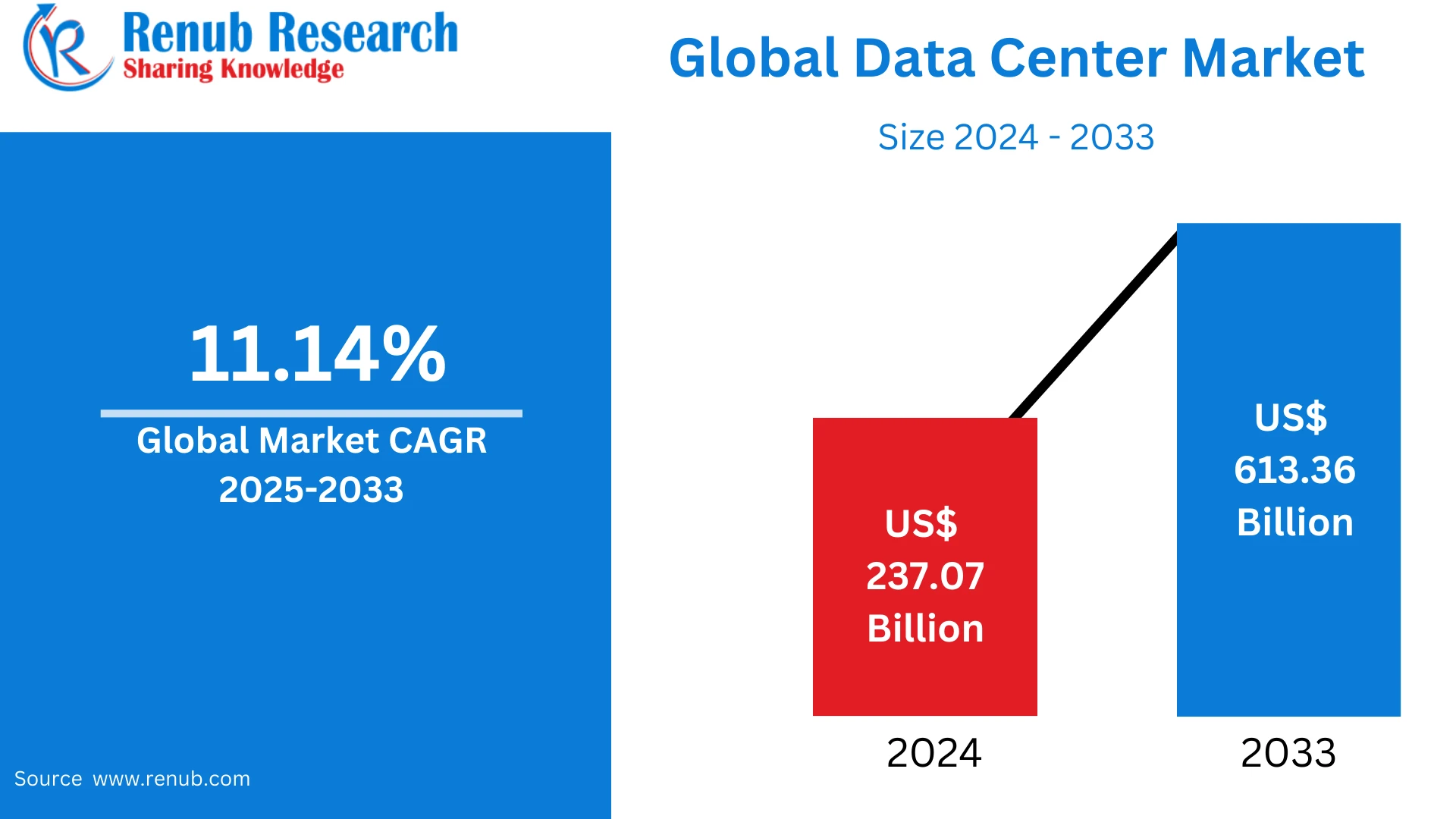

According To Renub Research global Data Center Market is entering a phase of accelerated expansion, driven by the exponential growth of digital ecosystems, cloud-based services, and data-intensive technologies. Valued at US$ 237.07 billion in 2024, the market is projected to reach US$ 613.36 billion by 2033, growing at a compound annual growth rate (CAGR) of 11.14% from 2025 to 2033. This remarkable growth trajectory reflects the increasing dependence of businesses, governments, and consumers on secure, scalable, and high-performance digital infrastructure. As organizations worldwide continue to digitize operations and adopt advanced technologies such as artificial intelligence, machine learning, and big data analytics, data centers have become the backbone of the global digital economy.

Download Free Sample Report:https://www.renub.com/request-sample-page.php?gturl=data-center-market-company-analysis-p.php

Overview of the Data Center Market

A data center is a purpose-built facility designed to house critical IT infrastructure, including servers, storage systems, networking equipment, and advanced security solutions. These facilities ensure the continuous processing, storage, and transmission of massive volumes of digital data. Modern data centers are equipped with redundant power systems, intelligent cooling mechanisms, high-speed connectivity, and sophisticated cybersecurity frameworks to guarantee maximum uptime and operational resilience. They play a vital role in supporting cloud computing platforms, enterprise applications, financial transactions, streaming services, and real-time data analytics.

The evolution of data centers has shifted from traditional on-premise models to highly automated, virtualized, and energy-efficient environments. Technologies such as software-defined infrastructure, AI-driven monitoring, and modular designs are increasingly adopted to improve scalability and reduce operational costs. As digital transformation accelerates across industries, data centers are no longer just storage facilities but strategic assets enabling innovation, agility, and global connectivity.

Key Drivers of Market Growth

The rapid adoption of cloud computing is one of the most significant drivers fueling the data center market. Enterprises are migrating workloads to public, private, and hybrid cloud environments to enhance flexibility, reduce capital expenditure, and improve performance. Hyperscale data centers operated by global cloud service providers continue to expand to meet the growing demand for compute and storage capacity.

Another critical growth driver is the proliferation of data-generating technologies such as the Internet of Things (IoT), 5G networks, artificial intelligence, and edge computing. These technologies generate enormous volumes of real-time data, necessitating robust and distributed data center infrastructure. Additionally, the rise of remote work, digital payments, e-commerce, and online entertainment platforms has significantly increased the need for reliable and secure data storage and processing solutions.

Data security and regulatory compliance also play a crucial role in market expansion. Organizations are investing heavily in data centers to ensure compliance with data protection regulations, maintain business continuity, and safeguard sensitive information against cyber threats.

Market Challenges and Constraints

Despite strong growth prospects, the data center market faces several challenges. High capital investment requirements for land acquisition, infrastructure development, and advanced cooling and power systems can act as barriers to entry. Energy consumption and environmental impact are also major concerns, as data centers are among the largest consumers of electricity globally.

Operational complexity, skilled workforce shortages, and the need for continuous upgrades to keep pace with technological advancements further add to market challenges. However, ongoing innovations in energy-efficient designs, renewable energy integration, and automation are helping mitigate these constraints.

Competitive Landscape and Leading Market Players

The global data center market is highly competitive, with a mix of infrastructure providers, technology vendors, and colocation service operators. Key players include Delta Electronics, Inc., Cisco Systems, Inc., Equinix, Inc., Fujitsu Limited, and General Electric. These companies focus on innovation, global expansion, and strategic partnerships to strengthen their market positions.

Hyperscale operators and colocation providers continue to invest in new facilities across emerging and developed regions to support growing digital demand. Technology vendors are emphasizing integrated solutions that combine power management, cooling, networking, and automation to deliver end-to-end data center efficiency.

Product Launches and Technological Innovation

Technological innovation remains central to market evolution. Hitachi, Ltd. has introduced advanced power architectures designed to support next-generation AI workloads, enabling more efficient and sustainable hyperscale data centers. These innovations address the limitations of conventional power systems by reducing energy loss and cooling requirements.

Similarly, Schneider Electric has expanded its modular and prefabricated data center solutions to meet the intensive demands of AI and high-performance computing. These solutions accelerate deployment timelines while enhancing energy efficiency and operational scalability.

SWOT Analysis and Strategic Strengths

Companies such as Siemens AG and Hewlett Packard Enterprise demonstrate strong competitive advantages in the data center market. Siemens leverages its expertise in energy management, automation, and smart infrastructure to deliver highly efficient and reliable data center solutions. Its focus on digital twins, predictive maintenance, and renewable energy integration positions it as a key enabler of sustainable infrastructure.

Hewlett Packard Enterprise benefits from a broad IT portfolio, including high-performance servers, storage, and hybrid cloud platforms. Its consumption-based models and edge-to-cloud capabilities support flexible, scalable, and energy-efficient data center deployments, making it a preferred partner for enterprises undergoing digital transformation.

Recent Developments in the Market

Strategic collaborations and technology advancements continue to shape the market. IBM Corporation has announced initiatives to explore distributed quantum computing in collaboration with Cisco Systems, Inc., highlighting the future role of data centers in supporting quantum networks.

Meanwhile, Dell Technologies Inc. has launched updated infrastructure solutions optimized for AI-driven workloads. These developments focus on improving performance, reducing costs, and enhancing sustainability across enterprise data centers.

Sustainability and Environmental Responsibility

Sustainability has become a strategic priority in the data center market. Aruba Networks, part of Hewlett Packard Enterprise, integrates energy-efficient architectures and AI-driven network optimization to reduce power consumption and environmental impact. Its approach emphasizes intelligent workload distribution and sustainable manufacturing practices.

Mitsubishi Electric Corporation focuses on high-efficiency power systems, advanced cooling technologies, and low-emission solutions. Through smart infrastructure and renewable energy integration, the company aims to achieve net-zero carbon emissions across its value chain while supporting eco-friendly data center operations.

Market Segmentation and Structural Analysis

The data center market is segmented based on component, data center type, industry vertical, and geography. Components include IT infrastructure, power solutions, cooling systems, and networking equipment. Data center types range from enterprise and colocation to hyperscale facilities.

Industry verticals such as BFSI, healthcare, IT and telecom, government, and retail are major contributors to demand. Geographically, North America leads the market due to early technology adoption, followed by Europe and Asia-Pacific, where rapid urbanization and digitalization are driving significant investments.

Historical Trends and Forecast Outlook

Historically, the data center market has evolved from centralized enterprise facilities to distributed, cloud-based ecosystems. The forecast period from 2025 to 2033 indicates sustained growth, supported by emerging technologies, expanding cloud adoption, and increasing focus on data sovereignty and security.

Market share analysis highlights the growing dominance of global infrastructure providers and technology vendors, while regional players continue to expand through partnerships and localized solutions.

Company-Level Strategic and Revenue Analysis

Leading companies such as Delta Electronics, Inc., Equinix, Inc., Digital Realty Trust, Inc., and CyrusOne Inc. focus on mergers, acquisitions, and capacity expansion to strengthen revenue streams. Investments in renewable energy, modular infrastructure, and advanced cooling technologies enhance long-term profitability and market resilience.

Future Outlook of the Data Center Market

The future of the data center market is defined by scalability, sustainability, and intelligence. As digital demand continues to rise, data centers will increasingly integrate AI-driven automation, edge computing capabilities, and renewable energy sources. The shift toward greener, more efficient infrastructure will not only reduce environmental impact but also improve operational performance and cost efficiency.

In conclusion, the global data center market is poised for robust growth through 2033. Supported by technological innovation, expanding cloud ecosystems, and sustainability-driven strategies, data centers will remain at the core of the global digital infrastructure, enabling the next generation of connected, data-driven economies.